|

The CEO of Japan Tobacco (JT), the world’s third-largest tobacco company, recently met with the Chairman of Vietnam’s Committee for the Management of State Capital (CMSC) Mr. Nguyen Hoang Anh in Hanoi and offered to participate in the equitization process of the Vietnam Tobacco Corporation (Vinataba). The Japanese firm has experience in transforming into a private company, as it was once a State-owned enterprise (SOE), and offered to share lessons learned so that Vinataba can improve its corporate governance and performance.

This is fully in line with the government’s ongoing efforts and strategy in recent years to speed up the equitization and divestment process at SOEs, though the country seems almost certain to miss its five-year plan for cutting State ownership in the economy by 2020.

Slow progress

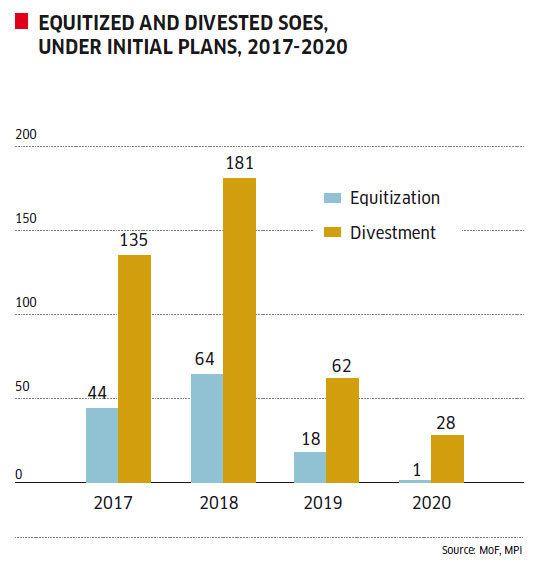

Prime Minister Nguyen Xuan Phuc issued Decision No. 26 on August 15 approving a new list of SOEs that should be equitized by the end of next year. The list adds 93 new SOEs to a previous list of 406 to be equitized by the end of this year, with a maximum of 65 per cent to be retained by the State. SOE equitization now stands at only 27.5 per cent of the government’s 2017-2020 plan, according to a report from the Steering Committee for Enterprise Innovation and Development.

Regarding divestment, in the first half of this year the government unloaded State capital from 30 SOEs to the tune of more than $119 million, bringing total divested capital to some $212 million. Of the 127 SOEs targeted for equitization this year, only 35 had done so as at the end of the first half. “The progress of SOE equitization has again fallen behind schedule,” said Ms. Nguyen Thi Vinh Ha, National Head of Advisory Services at Grant Thornton Vietnam. “It’s quite apparent that the government will again not meet its SOE equitization target in 2019.”

The new Decision No. 26 clearly allocates responsibility for the equitization process, from the level of ministries down to SOEs’ management, with quarterly reporting required to the Prime Minister and the Ministries of Finance (MoF) and Planning and Investment (MPI). Ms. Ha believes there will be a stronger push seen in equitization in the time to come.

However, with just 15 months or less to complete equitization, in Grant Thornton’s opinion the task will be quite challenging owing to the fact that some of the barriers that have slowed down the process in the past remain unsolved, together with the introduction of stricter regulations, including auditing requirements in projects where the State has invested in excess of $73 million.

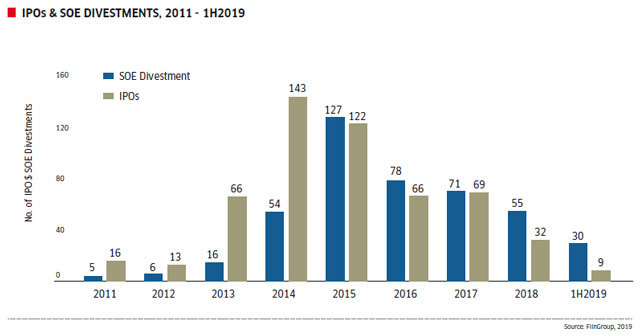

There have been virtually no State divestments or initial public offerings (IPOs) this year, while the country has posted one of the busiest IPO seasons in Southeast Asia over the last two years.

To improve economic efficiency, according to Mr. Le Anh Tuan, Deputy CIO at Dragon Capital, IPOs and SOE restructuring are a must. “This will also help to deepen the financial market, so we hope to see more significant IPO activities with a clearer structure in terms of asset valuation and tax determination, and better pricing, which will draw investors’ attention,” he told VET. “Usually, they would also like to have exposure to final consumer spending. Therefore, Satra, MobiFone, Vinaphone, the Vietnam Cement Industry Corporation (Vicem), and Saigontourist, to name just a few, are of more interest.”

|

|

|

Opportunities missed

Though equitization of large SOEs brings a large pool of potential opportunities to investors, if upcoming IPOs become unattractive to private investors then poor business performance will be a major factor. Examples include Vinataba, Genco 2, Vicem, and the Saigon Industry Corporation (CNS).

However, Ms. Ha from Grant Thornton Vietnam said that poor performance alone is sometimes not an issue. “In fact, in many cases, changing ownership, management, and strategy can bring new opportunities to turn the business around,” she said. “Poor performance becomes worse when it is added to the still high holding of the State post-IPO and the limit on strategic foreign ownership. With the presence of such factors, private investors controlling and changing the business will be problematic, if not impossible, and this makes such investments unattractive.”

She added that the slow progress of SOE equitization and divestment is believed to have resulted not only in missed opportunities but also damaged credibility. The first obvious opportunity that Vietnam may have missed due to the delayed process was the chance to IPO good SOEs in the booming stock market of 2018. If the pace of IPOs and divestment was faster, more SOEs would have had IPOs last year, would have mobilized a large amount of money or sold State capital at a higher price, and Vietnam would have gained more capital from global funds.

Many analysts have commented on certain factors dissuading private investors from buying shares in SOEs, including valuations and the lack of a transparent “due diligence” process. Taking Sabeco as an example, a liability to the State of nearly $108 million was discovered after its equitization in 2017 and remains unresolved. Taking into account this contingent liability, would Sabeco have had such a high valuation? This reinstates the concerns of foreign investors about a lack of transparency in information disclosure during the divestment process that does not allow them to determine potential risks at and value of SOEs when making investment decisions.

From a State economic management point of view, owning a continuously loss-making company is not good for any government. Therefore, regardless of the form of divestment, it is by nature better for the economy and the State budget. Better transparency would get a better price, and a public auction with a major stake offering would make it more attractive.

There are two types of IPOs: one for price discovery, with some 20 per cent offered to the market to determine how much the market is willing to pay, and another a significant stake divestment with possible management handover in order to transform the company. “In the case of price discovery, and most Vietnamese IPOs belong in this category, what we sense is that the government is putting price as the top priority rather than a wish to transform the business and improve efficiency,” Mr. Tuan from Dragon Capital noted.

An IPO not followed by a listing is like an engagement not followed by a wedding. Mr. Tuan therefore suggested the government impose strict HSX or HNX listing, as UPCOM is not recognized as an exchange. Furthermore, listing conditions and related paperwork, including accounting and legal issues pre-IPO, must be resolved as soon as possible. An example is Airports Corporation of Vietnam (ACV), which was equitized in 2015 but seen listing continuously delayed.

|

|

|

Determination needed

The success of the equitization of these SOEs will need further effort from the SOEs themselves and greater support from the government and relevant ministries to streamline the process. In order to call for investment in SOEs that are recording poor business performance, the government needs an attractive investment offer and could consider offering tax incentives or a better price.

The missed opportunities are adding up. Given the US-China trade war, according to Ms. Nguyen Lan Phuong, Partner at Baker & McKenzie Vietnam, if Vietnam does not act promptly it will miss the chance to capture a quick and strong inflow of FDI, to enhance the prestige and capability of the country and its government in the international community, and for domestic companies to integrate into global supply chains.

In terms of the State divestment strategy, she emphasized, the opportunity to take benefits from the most valuable assets of both sides is a lost opportunity. The State is missing out on private capital sources and, more importantly, the governance and management expertise of the private sector. The private sector, meanwhile, is missing out on the opportunity to participate in some of Vietnam’s most strategic industries and enterprises.

“The mismatch in expectations on both sides - SOEs and the government and the private sector - in terms of due diligence, valuation, and growth direction of the business post-equitization is a major hindrance,” Ms. Phuong added. “Government agencies have not yet adopted a pro-business attitude, and generally speaking the private sector requires more certainty and transparency in the equitization process for them to participate strongly.”

Though the size of Vietnam’s stock market has doubled annually and become more attractive to investors, the banking system remains the most important channel for capital funding, according to Ms. Nguyen Hoang Kim Oanh, Partner at Baker & McKenzie Vietnam. The government, therefore, should grow the market and lure more SOEs to list shares through speeding up their equitization.

In addition to suggestions about a merger of the two stock exchanges, HSX and HNX, she recommended the legal framework be completed to improve the transparency of corporate information disclosure, and if the government could consider the difficulties investors face and offer proper action, it would enhance the equitization of the SOEs. Further, the management of to-be-equitized SOEs should commit to cooperation during the process to speed up and enhance its success. VN Economic Times

Khanh Chi

Building credit: How SOEs can get foreign financing for infrastructure

State-owned enterprises (SOEs) face unique challenges when it comes to attracting foreign financing for infrastructure projects. But there are solutions.

Vietnamese SOEs’ outward investment projects take big losses

The losses incurred by state-owned enterprises (SOEs) from outward investment projects in 2018 reached $367 million, a sharp increase of 265 percent compared with 2017, a report shows.