|

It is expected the credit growth ceiling for FE Credit and HD Saison, major finance firms in Vietnam’s market, will be limited to a lower level (compared to respective 20% and 35% in 2018).

Military Bank’s financial arm MCredit, a relatively small player with around 6% market share that quadrupled loans last year received a credit growth quota of 37%, far below what the company had hoped for. Military Bank (MBBank) had to reduce its target of MCredit's contribution to consolidated earnings from above 6% to only 4% due to the SBV’s decision.

In 2019, SBV set credit growth target for the whole system at 14%, equivalent to the actual level achieved in 2018. However, it can be adjusted according to market and macro-economic conditions. In other words, the SBV continues to control credit closely after keeping 2018 credit growth at 14%, the lowest level in the past five years.

According to VDSC, domestic credit still grows faster than nominal GDP in Vietnam and that could pose some risks in the long-term. After several years of high credit growth, domestic credit to the private sector has risen to 130% of GDP from just 20% some 20 years ago.

International institutions such as the IMF and WB suggest credit growth needs to slow down to maintain macro-economic stability. Therefore, VDSC stated a lower credit growth target, as announced by the SBV, is appropriate.

Banks’ compliance progress on credit growth

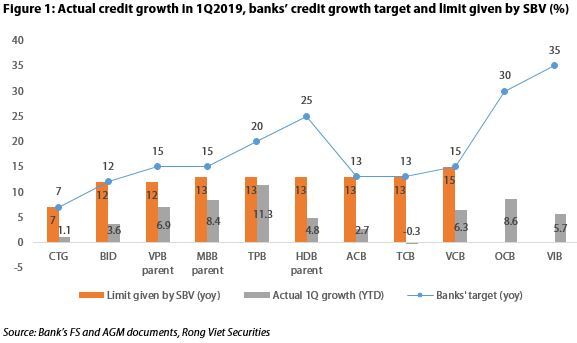

In recent years, the SBV gave each bank an initial credit growth ceiling in the first quarter. Then, based on the actual macro-economic conditions, the SBV might raise credit limits for certain banks in the last quarter. In 2018, the initial quota granted to most banks was 14-15%, and after that in the fourth quarter, the limit was raised to around 18-20% for some.

For 2019, as per banks' information, the majority were allocated an initial credit growth limit of 13%, including Asia Commercial Bank (ACB), MBBank, Ho Chi Minh Development Bank (HDBank), TienPhongBank (TPBank), and Vietnam Technological and Commercial Joint Stock Bank (Techcombank).

Some lenders were given lower quota including Bank for Investment and Development of Vietnam (BIDV) (12%), Vietnam Prosperity Bank (VPBank) (12%) and Joint Stock Commercial Bank for Industry and Trade (VietinBank). In contrast, Joint Stock Commercial Bank for Foreign Trade of Vietnam (Vietcombank), one of the first three banks that fully complied with Circular 41, was assigned a slightly higher figure, 15%.

Before that, the SBV had stated that banks complying with the new capital adequacy requirements early would be awarded priority in credit growth as well as transaction network development. As such, it is expected that the other two early adopters, including Vietnam International Bank (VIB) and Orient Commercial Bank (OCB), will be granted a higher credit ceiling, but that has not been finalized yet.

By April 2019, there were four more banks certified for having complied with Circular 41, which are MBBank, ACB, TPBank and VPBank.

Circular 41, one of the regulation documents for Basel 2 criteria, stipulates that banks and branches of foreign banks must regularly maintain the CAR determination based on their financial statements of at least 8%. The circular will take effect as of January 1, 2020.

They will start applying the new capital adequacy standards from May 01, 2019. Thus, a total of seven banks have now been recognized as early adopters and expect the SBV will raise their respective credit growth quota. Others hope to join soon. Techcombank, one of the pilot banks for Circular 41 and HDBank have applied and expect to receive approval within this quarter.

This is the reason why many banks set higher (than 13%) credit growth targets at their annual general meetings including MBBank (15%), VPBank (15%), TPBank (20%), HDBank (24 %), OCB (30%) and VIB (35%). Others are more conservative (for now), including Vietcombank (15%), Techcombank (13%), ACB (13%), BIDV (12%) and Vietinbank (7%). It is expected BIDV and Vietinbank will at best achieve the quota due to current capital constraints.

For this year, many banks were or will be certified as fully complied with Circular 41 early adoption, with much stricter capital requirements than current regulations. As such, VDSC said it would be more reasonable to let these banks manage their own credit limits, providing all safety limits and ratios are met. This will facilitate more appropriate credit allocation and motivate banks to improve lending quality to achieve deserved credit expansion quota. Hanoitimes

Hai Yen