The State Bank of Vietnam (SBV), the country’s central bank, has managed its macro-economic targets in a way that is conductive to foreign direct investment (FDI) and the resilience of the economy, according to HSBC Vietnam.

|

|

The central bank's policies have largely helped the social and macro stability

|

The SBV’s targets are around inflation and social and macro stability due to the disruption of the supply chain in the first half of 2020 caused by unprecedented Covid-19, combined with significant volatilities in the global financial market, said CEO of HSBC Vietnam Tim Evans.

Monetary policy in 2020

Since the beginning of the year, SBV has proactively cut key policy rates and to ensure sufficient liquidity in the financial system.

During the first 11 months of the year, the SBV has reduced policy rates for three times, in order to provide support for financial institutions to have alternative access to funding at lower cost.

The SBV also reduced 0.6%-0.75% per annum (p.a) on the deposit ceiling rate for deposits of below six-month tenor; and reduced 1% p.a of lending ceiling rate for short term loan in the priority areas which helped lead to a speedier recovery of the local economy.

In terms of foreign exchange (FX) management framework, the SBV continued to provide timely support and guidance, in order to ensure stability and sustainable development of the market in overall.

For instance, SBV provided two-way support when it lowered the US dollar selling rate in in March to meet legitimate demands as when FX market appeared to be under pressure during the social distancing period, and lower the USD buying rate in November when dollar supply in the market turned ample again.

Unlike previous years when the dong usually depreciated against the greenback, in 2020 dong has even appreciated slightly by about 0.2% compared to the follar, while there has been almost no year-end pressure for the FX market, Tim Evans noted.

|

|

CEO of HSBC Vietnam Tim Evans

|

Fiscal policy

While Vietnam has emerged stronger from Covid-19 than other regional peers, its economy, nonetheless, needs support for those hard-hit businesses and consumers.

Although Vietnam is unable to implement sizeable fiscal stimulus packages, it has introduced some targeted and short-term assistance, mainly consisting of tax deferrals and direct cash hand-outs to poor households.

Vietnam’s Ministry of Planning and Investment has recently proposed a second stimulus package, consisting of financial support for aviation (worth VND11 trillion or US$478 million) and tourism sectors, as well as more direct cash hand-outs of VND3.6 trillion.

The government is expecting a budget deficit to 5-5.6% of the GDP, over the initial target of 3.4%. In the 2021-25, the government sets a target of average budget deficit of around 3.7%, specifically 4% in 2021 before reducing to 3.4% in 2025.

It’s notable that the government has made a humble target of 1.4% increase in spending for infrastructure in 2021. This shows a possibility of government not using public budget to finance big infrastructure projects but using PPP instead, which is an ideal model for Vietnam to balance between an ambitious infrastructure development target and a narrow fiscal budget.

In fact, the government has sought bilateral and multilateral support from the US, Japan, Australia and the WB.

|

|

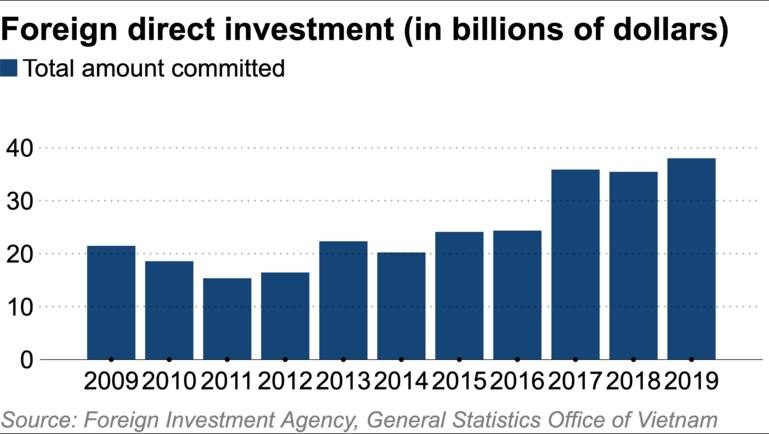

FDI to Vietnam for years

|

Things to note

Tim Evans noted that the Covid-19 crisis continues to have a negative impact on the global economy, pressure on state budget will increase as the result of lower revenue, while higher spending due to the government’s increasing stimulus package could mitigate the negative effect of pandemic on households and businesses.

Even though Vietnam remains a bright star for growth, the CEO sees some challenges if the government does not take timely actions and seize opportunities.

Accordingly, the first issue which has been raised in recent years, even though remarkable progress have been made, the government should continue to push the equitization of state-owned enterprises (SOEs) as SOEs still dominate one-third of the entire economy today. The equitization of SOEs will help reallocate investment capital, liberating labor productivity, and supporting economic growth.

Secondly, according to the World Bank, Vietnam's infrastructure investment as a percentage of GDP is among the lowest in the ASEAN region. This creates challenges for the continued growth of modern infrastructure services that are required for the next phase of growth (Vietnam is ranked 89th out of 137 countries for quality of its infrastructure).

The third point relates to FDI which is also one driving force for Vietnam's development. As mentioned above, FDI’s sustainable growth is one of the points to be proud of, but it would be even better if the government improves customs and administrative procedures, which are factors hindering the development of this industry.

The last thing is regarding sustainable growth. Vietnam’s rapid growth and industrialization have had detrimental impacts on the environment and natural resources.

With demand for production and domestic use, total electricity consumption has grown faster than electricity output.

Strategies and plans to promote green growth and the sustainable exploitation of natural resources have been adopted and it is very encouraging to see the openness of many Vietnamese businesses that when it comes to sustainable development, HSBC Vietnam CEO emphasized. Hanoitimes

Central Bank expected to cut key rate to aid economy

The inflation in 2020 is forecast at 3.3%, significantly lower than the target of 4% set by the government.

A strange move initiated by the central bank

The State Bank of Vietnam (SBV) has issued decisions No. 1349 and 1351 on cutting interest rates applicable to compulsory reserves deposited at the central bank by credit institutions,