South Korea’s KEB Hana Bank in July successfully acquired a 15 per cent stake for around $878 million in the State-run Bank for Investment and Development of Vietnam (BIDV), the country’s largest lender by assets, making it the largest foreign-invested merger and acquisition (M&A) deal in Vietnam’s banking sector to date.

It is one of many other deals wrapped up recently amid a continuing influx of foreign investment into Vietnam.

M&As in the banking sector are forecast to become commonplace in the near future as many banks are accelerating their restructuring and raising capital to meet the deadline on Basel II standards by 2020, as set by the central bank.

Deals abound

M&As deals in the local banking sector this year are estimated to have totaled some $2 billion.

Prior to the BIDV and KEB Hana Bank deal, the Bank for Foreign Trade of Vietnam (Vietcombank) early this year increased its charter capital to $1.6 billion by selling a combined 3 per cent stake (equivalent to over 111 million shares) in a private placement to Japan’s Mizuho Bank and Singapore’s sovereign wealth fund GIC for a total value of $268 million.

These two deals injected substantial capital into two of the country’s leading banks and helped them fulfill their roles as major lenders in the economy.

Many private banks also have plans to seek out strategic or financial investors. Military Bank (MBBank) plans to trade 7.5 per cent of charter capital to a number of financial investors this year, while Vietcombank is continuing with a plan to issue another 6.5 per cent of shares this year and next to foreign investors.

And not only large banks are courting foreign investors, as smaller banks like the National Citizen Bank (NCB),VIB, OCB, and Nam A Bank are also looking for strategic investors, according to Ms. Nguyen Thi Thuy Anh, Banking Analyst at the Viet Dragon Securities Company (VDSC), and this wave will be stronger next year as the deadline for banks to list approaches.

Weaker banks undergoing restructuring are also moving ahead with M&A plans. Ocean Bank is entering the final stage of a sale to an Asian bank, while Japanese investment management firm J Trust has expressed a willingness to become involved in the restructuring of poorly-performing credit institutions in Vietnam and to buy the Vietnam Construction Bank (CBBank).

In addition, the Global Petro Commercial Joint Stock Bank (GPBank) is currently strengthening its performance and some foreign investors are interested in a long-term cooperative deal.

Having observed this year’s M&A activities in the banking sector, Mr. Long Ngo from the Viet Capital Securities Company (VCSC) concluded that foreign money still prefers stakes in larger banks over hunting for smaller bargains.

Whether it’s GIC’s attraction to the sizeable Vietcombank with one of the largest active customer bases in Vietnam or KEB Hana’s attraction to BIDV with arguably the largest bricks-and-mortar operation in the country, size does seem to matter.

Domestic buyers of banking assets are few and far between and deals that have to rely predominantly on domestic investors, such as TPBank’s new primary issue or ACB’s attempt to sell its treasury shares, are finding it difficult to clear deals.

It can’t be denied that Vietnamese banks are becoming more attractive in the eyes of foreign investors after a drastic process of restructuring and addressing bad debts, with positive business results posted in 2018 and the first half of 2019, Mr. Giles T. Cooper, Co-General Director of Duane Morris Vietnam, said.

The country’s banking sector has shown significant improvement, partially as a result of stable inflation figures and interest rates and strong FDI.

Opportunities ongoing

|

|

|

In the context of continued foreign direct and portfolio investment inflows into Vietnam, there are favorable conditions for M&A deals to flourish. With significant trade and legislative developments in 2018 and 2019, such as the CPTPP, the EVFTA, and the EVIPA Investment Protection Agreement, and more to come, such as amendments to the Investment Law, Enterprise Law, and Securities Law, not to mention the benefits from the rift in China-US relations, Vietnam is well placed to attract more investment, including investment capital flows through M&A deals, and this will have an even greater positive impact on the banking and finance sector.

Mr. Cooper sees many opportunities in the near and medium term. “Weak banks need capital to accelerate their restructuring plans, and many State-owned and commercial banks need to increase their Tier-2 capital, maintain their capital adequacy ratios, tap new foreign currency sources for foreign currency loans, and improve technical, management, and strategic business plans,” he said. “All of this opens up opportunities for investors.”

In particular, the banking sector is normally the first sector foreign investors look at given its important role in the economy and the decent market capitalization of most players, according to Ms. Thuy Anh from VDSC.

While many Western investors withdrew during 2017-2018, existing Asian investors have maintained their holdings in Vietnamese banks and many investors from South Korea, Japan, Thailand, and Singapore are looking to increase their stakes.

Thanks to cultural similarities and geographic advantages, Asian investors seems to dominate investment in Vietnam’s banking sector these days.

Notably, financial corporations from South Korea are actively looking for investment opportunities in Vietnam amid limited domestic investment opportunities and strong collateral relationships between the two countries. In addition, M&As are a method for them to implement their international expansion strategies. In the case of KEB Hana Bank, globalization is a strategic focus and expanding into Vietnam is defined as part of that strategy.

Mr. Long from VCSC said the local banking sector is attractive because of commonly-known factors such as low banking penetration, an excellent macroeconomic backdrop, firm pricing on the interest income side, and a system playing catchup on banking related fees such as bancassurance and settlement services relative to what regional economies deliver.

“South Korean financial institutions are particularly attracted to the chance to follow large South Korean corporate customers as they increase their investment in Vietnam and are comforted by the strong macro backdrop, as this element is critical to minimizing the probability of encountering a new bad credit cycle,” he said.

He added that strong top-line and bottom-line growth across banks under VCSC’s coverage reaffirm a belief among investors that the banking sector is an excellent proxy to track the overall strength of Vietnam’s economy.

Most banks looking to raise money in the next 12 months are relying primarily on foreign investors and this makes deals more likely.

Private banks that raised capital in 2017 and 2018 are under less pressure to raise fresh capital but may tap into the market on an opportunistic basis if share prices return to IPO levels, which is the case at VPBank, for example.

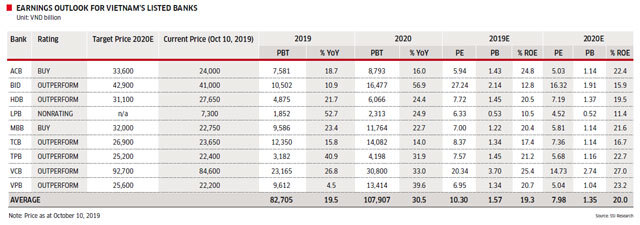

On the other hand, the fundamentals at Vietnamese banks have been enhanced in general and listed banks have delivered strong growth in earnings over recent years, according to SSI Research. Eleven banks have been permitted to officially apply Basel II standards.

Asset quality has been improving, with banks’ making major efforts to resolve legacy bad debts and keep new non-performing loans (NPLs) at low rates.

Local banks now have an increasing ability to leverage growth through technology and data experience in a fast-growing market with a customer base boasting substantial potential. SSI has forecast that listed banks in Vietnam under its coverage are expected to deliver strong growth in earnings in 2019-2020.

Rocky road

Many analysts believe that M&A activities at local banks will continue to be robust in the coming years as the foreign ownership limit (FOL) in the banking sector will continue to be raised and State ownership will continue to decline at State-owned commercial banks.

Nevertheless, local banks that have already hit their maximum FOL such as Vietinbank, TPBank, and ACB, will be unable to raise fresh capital in large volumes until the government passes the pending Securities Law later this year and moves to lift the FOL when the legislation takes effect at the beginning of 2021, Mr. Long noted.

Also, Basel II is just one step in the process of harmonizing the regulatory approach to international standards, and another key step is for all banks to begin producing IFRS9-compliant accounts. This will make the task of evaluating Vietnamese banks much easier for foreign investors.

Banks of large and medium size, with healthy asset quality, strong profitability, and financial transparency are likely to attract more foreign investors.

Conversely, those with limited earnings potential, poor asset quality, and weak corporate governance will face more challenges seeking investors.

However, as the government has attempted to facilitate the restructuring of weak banks and limit the issuing of new licenses for foreign banks in Vietnam, foreign investors can also consider M&As with these weak institutions as an option in strategies to enter Vietnam.

In fact, it’s still difficult for weak banks to restructure because the process of collecting bad debts, despite the existence of Resolution No. 42, still has some challenges, and the support of weak banks is based largely on State-owned banks, who also have to deal with their own problems, according to Ms. Thuy Anh.

She also sees some challenges for foreign investors in acquiring stakes in local financial institutions. Firstly, the FOL is at 30 per cent and most healthy listed banks have no more room left.

Those with some room left are already expensive. Second is complicated bureaucracy and constraints from legal regulations.

The deal between KEB Hana Bank and BIDV took much longer than expected due to price and procedural issues.

Finally, the weaknesses of some players, including low asset quality, poor corporate governance, and low financial transparency, safety, and security are hindering foreign investors’ decisions. VN Economic Times

Hung Cao

Vietnam’s banking sector becomes more attractive to investors

Growing attractiveness of Vietnamese banks' shares is thanks to a positive revamp and strong outlook of the sector, particularly as Vietnam is accelerating global economic integration.

EVFTA gains in Vietnam's telecoms and banking

Even though a bigger lift in foreign ownership cap could become a driving force to lure further European investment in banking and telecommunications, the funding picture in these sectors remains a question.