|

| Source: State Bank of Vietnam, Fitch Solutions |

Fitch Solutions, a research unit of Fitch Group, blamed the deceleration in loan growth for the State Bank of Vietnam (SBV)'s lower loan growth target set for 2019 in comparison to the previous year, the transition to Basel II standards by January 1 2020, and a slower economic growth environment.

Given these, the research entity expects loan growth to slide to 13 per cent in 2019, from 14 per cent in 2018.

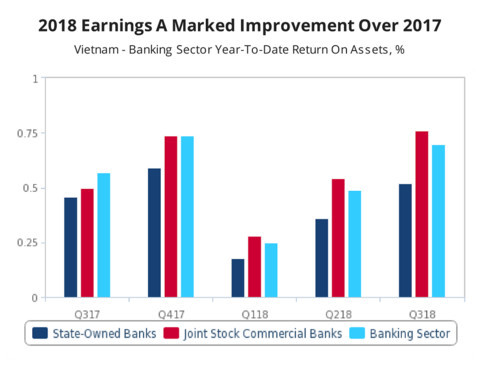

The profitability of Vietnamese banks has been steadily improving as the return on assets for the banking sector in the third quarter of 2018 significantly outperformed the comparable period in 2017.

Although aggregate measures have yet to be published by the SBV, Fitch Solutions expects the numbers to show an impressive year for the banking sector. Agribank, Vietnam’s largest state-owned bank by assets, posted the highest profits in its history, with a pre-tax profit of VND7.5 trillion (US$323,000), up 50 per cent from VND5 trillion (US$215 million) in 2017.

Other state-owned banks such as Vietcombank and BIDV also enjoyed a record 2018 with their respective pre-tax profits reaching VND18 trillion (US$776,000) and VND9.6 trillion (US$414,000), surging by 63 per cent and 11 per cent on year, respectively.

Sacombank, a joint stock commercial bank, also saw a 47 per cent jump in profits relative to 2017 to VND2.2 trillion (US$95,000) in 2018.

Loan growth under pressure

Fitch Solutions expects a slower pace of loan growth to weigh on earnings during 2019. This will primarily be attributed to three factors.

Firstly, the SBV has set a credit growth target for the overall banking sector to be 14 per cent in 2019, the same as the rate achieved in 2018, but lower than the 17 per cent credit growth target initially set for the previous year.

In 2019, banks which have met Basel II standards earlier than the SBV’s 2020 deadline will be allocated a credit growth limit of 15 per cent, with the rest being allocated a limit of below 12 per cent.

In comparison, most banks were assigned relatively higher credit growth limits between 14-16 per cent in 2018. Secondly, the incorporation of Basel II standards requires that banks to meet a capital adequacy ratio (CAR) of 8 per cent.

Although the CAR of state-owned banks and joint stock commercial banks, which together account for 85 per cent of assets in the banking sector, are already at 9.3 per cent and 10.6 per cent, respectively, the calculation for risk-weighted assets will be stricter under Basel II standards. This could make the CAR of these banks fall, Fitch Solutions predicts.

Thirdly, the country’s economic growth is unlikely to be spared from the synchronized global economic slowdown with real GDP growth forecast at 6.5 per cent in 2019, a drop from 7.08 per cent in 2018. Fitch Solutions predicts that slowing economic activity amid a bleaker growth outlook will begin to weigh on credit demand over the coming quarters.

Capitalization remains an issue with Basel II implementation

The research firm noted that many Vietnamese banks, particularly smaller ones will face the problem of undercapitalization when Basel II standards are implemented due to a more stringent calculation of risk-weighted assets. This could see consolidation in the sector involving smaller and weaker domestic banks with larger counterparts needed to attain the required capitalization levels.

The government could also relax restrictions on foreign ownership to incentivize foreign banks to inject capital into the banking system.

Currently, foreign banks face a cap of 30 per cent on their ownership in domestic banks, which makes it challenging for them to gain managerial control. And this has impeded foreign investment in local banks.

Having managerial control of domestic banks is important for foreign players as most domestic banks have endured a combination of poor operations and poor management. This has resulted in a growing number of foreign banks preferring to set up a 100 per cent foreign-owned bank, rather than trying to purchase its own stake in a local bank.

To meet the SBV’s deadline for the Basel II implementation by 2020, local banks have been asking the government to approve the foreign ownership cap to 49 per cent with the hope of attracting foreign capital.

An ownership cap of 49 per cent would still allow the government to own 51 per cent of banks and control them through the Law of Credit Institutions and other legal regulations if needed, making it a possible scenario for banks facing capitalization issues when the implementation of Basel II standards kicks in.

VOV