|

| Unloading containers at Cat Lai Port, Ho Chi Minh City. (Photo: VNA) |

The Ministry of Industry and Trade (MoIT) last week reported to the government that in July, total export turnover was estimated to sit at $29.68 billion, up 0.8 per cent on-month. Domestically invested exporters earned $7.76 billion, down 1.8 per cent; and foreign-invested exporters came at $21.92 billion, including crude oil exports up 1.7 per cent. Also in July, the total import and export turnover of goods was estimated at $57.21 billion, up 2.5 per cent over the previous month and down 6.7 per cent over the corresponding period last year.

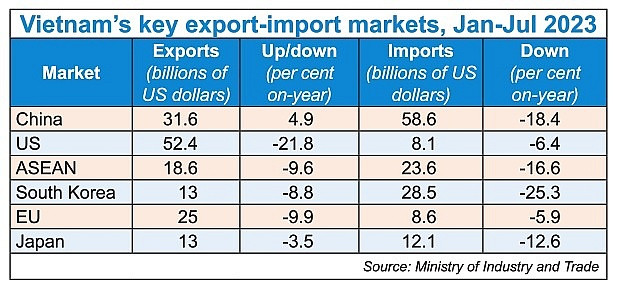

Cumulatively, in the first seven months of this year, the country’s total export value hit $194.73 billion, down 10.6 per cent as compared to that in the same period last year. However, the MoIT said that this reduction is being narrowed down as it remains lower than the on-year reduction of 12.1 per cent in the first half of this year.

Under the General Statistics Office’s Q2 survey on enterprise performance, when it comes to orders, almost three-quarters said they expect a rise and stability in orders in Q3 as compared to Q2. Only just over one-quarter of respondents predicted a reduction in orders.

As for export orders, 73 per cent of enterprises said they expect a rise and stability in orders in Q3 as compared to Q2. Only 27 per cent projected a decrease in export orders.

One of the strong foundations for the respondents to believe in a brighter export outlook is that good signals from the major export markets, said the MoIT.

American multinational financial services firm J.P. Morgan also stated, “The US has avoided recession so far in 2023. The US economy, as measured by real GDP, has expanded at an estimated 1.5 to 2 per cent annualised pace through the first half of the year. While business sentiment has been downbeat and business investment has slowed, the upside to consumer spending has provided a positive offset.”

|

Meanwhile, the EU has also been boosting implementation of its NextGenerationEU, an €806 billion ($886.5 billion) temporary recovery instrument to help repair the immediate economic and social damage brought about by the pandemic.

However, according to the MoIT, though Vietnam’s export situation is regaining momentum, it is expected to face massive difficulties in the months to come due to the world economy forecasted to see slower-than-expected growth, leading to a slow-paced recovery in consumption demands.

More than a week ago, the International Monetary Fund issued its fresh forecast on the global economy outlook. “Global growth is projected to fall from an estimated 3.5 per cent in 2022 to 3 per cent in both 2023 and 2024. The rise in central bank policy rates to fight inflation continues to weigh on economic activity,” it said.

All regions worldwide are also predicted to see lower-than-2022 economic growth in 2023, such as the US (1.8 per cent for 2023 versus 2.1 per cent last year), the euro area (0.9 per cent versus 3.5 per cent), Japan (1.4 per cent versus 1 per cent), and other advanced economies (2 per cent versus 2.7 per cent).

This grey forecast would also mean demands for goods will not be able to bounce back remarkably from now until the year’s end, affecting Vietnam’s efforts to boost exports, according to the MoIT.

In the first seven months of this year, Vietnamese enterprises’ export turnover hit nearly $51.5 billion or an on-year reduction of 10.2 per cent – accounting for 26.4 per cent of the economy’s total export value. Foreign exporters’ export turnover including crude oil stood at nearly 143.23 billion, down 10.8 per cent on-year and creating 73.6 per cent of Vietnam’s export turnover.

The economy witnessed a seven-month trade surplus of $15.23 billion, not deemed a good signal as both exports and imports suffered from on-year value reduction at 10.6 and 17.1 per cent, respectively, especially in the current context that Vietnam is a trade-reliant economy.

Source: VIR