Vietnam’s stock market opened the week with a sharp decline as negative sentiment spread from major global financial centers.

By the end of the morning session on June 8, the VN-Index had fallen nearly 39.7 points, or almost 2.2%, slipping below the 1,800-point mark. The HNX-Index lost nearly 3.2%.

Liquidity on the Ho Chi Minh City Stock Exchange remained weak, with trading value reaching just over VND8 trillion (USD307.7 million), reflecting cautious investor sentiment and fading market momentum.

Vietnamese stocks fall amid global sell-off

Selling pressure was broad-based, particularly among large-cap stocks.

Shares linked to the Vingroup ecosystem came under heavy pressure. VIC dropped VND9,000 to VND198,000 per share, while VHM lost VND4,900 to VND147,100. VPL declined VND1,600 to VND89,900 per share.

Banking stocks also traded deeply in negative territory. Other major blue-chip names, including FPT and VJC, posted significant losses, reducing the market value of some of Vietnam’s wealthiest investors.

The decline in Vietnamese equities mirrored a broader downturn across Asia-Pacific markets.

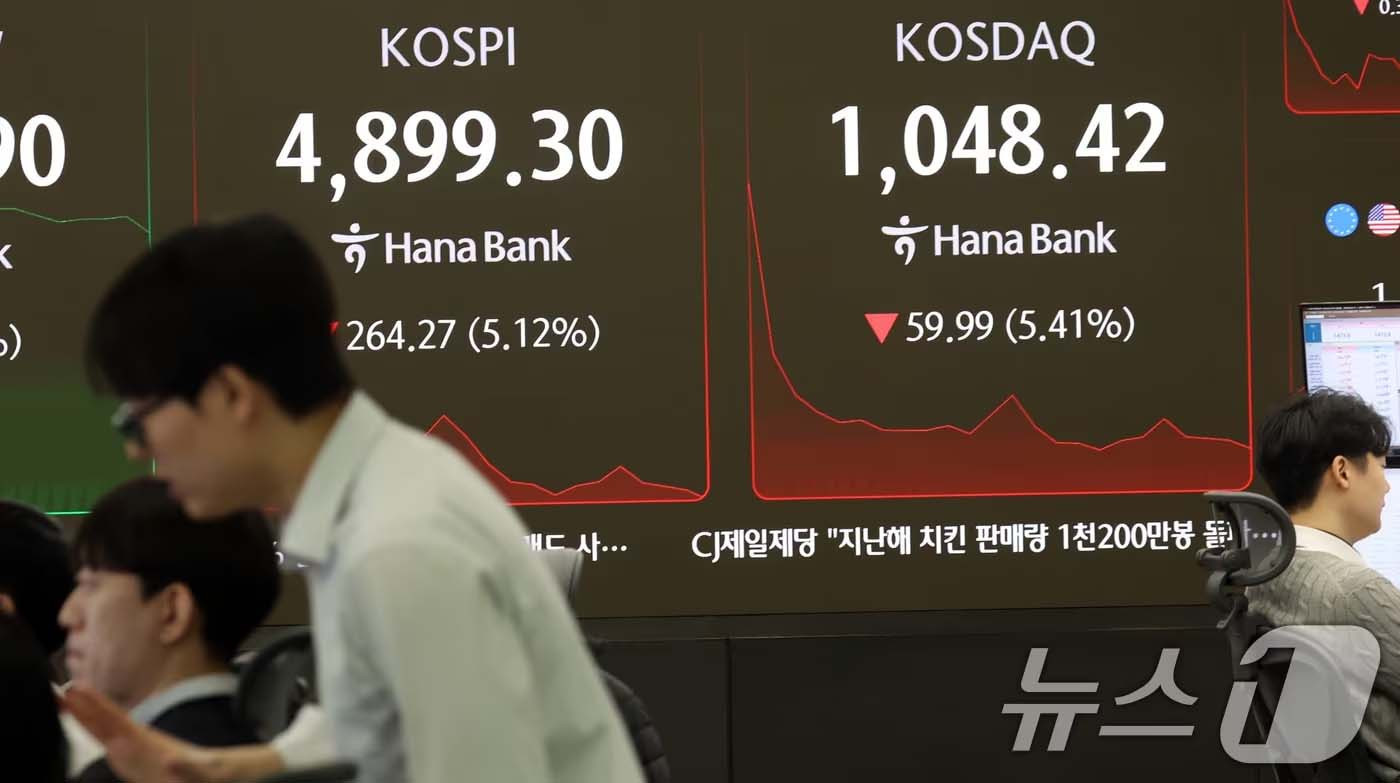

South Korea’s Kospi index plunged more than 8% at one point, forcing the Korea Exchange to activate a circuit breaker and temporarily halt trading for 20 minutes to curb panic selling.

At the same time, Japan’s Nikkei 225 fell 4.6%, Hong Kong’s Hang Seng Index dropped nearly 2%, and China’s CSI 300 lost about 1.5%.

Wall Street shock reverberates worldwide

The turbulence followed a dramatic sell-off in the United States at the end of last week.

The Nasdaq Composite dropped more than 4%, marking its steepest one-day decline in over a year. The S&P 500 fell 2.64%, while the Dow Jones Industrial Average lost nearly 700 points.

In a single trading session, approximately USD2 trillion in market capitalization was erased from Wall Street.

One of the primary catalysts was a stronger-than-expected US employment report. The American economy added 172,000 jobs in May, roughly double market expectations.

The data fueled concerns that the US Federal Reserve may keep interest rates elevated for longer and potentially maintain a tighter monetary stance if inflationary pressures persist.

A notable feature of the market reaction was that both equities and gold declined sharply at the same time.

Meanwhile, the US dollar climbed to its highest level in several months, suggesting global capital is increasingly seeking refuge in dollar-denominated assets.

Growing pressure on Vietnam and emerging markets

Recent developments indicate investors are entering a more cautious phase after months of optimism driven by artificial intelligence-related enthusiasm and expectations of Federal Reserve rate cuts.

One emerging trend is the apparent return of global capital to the United States.

With US Treasury yields rising toward 4.5% annually, many investment funds are reducing exposure to emerging markets and reallocating capital to the US, where yields are attractive and perceived risks are lower.

South Korea has already become a clear example of this shift. The Korean won recently fell to its weakest level in 17 years as foreign investors continued withdrawing funds from local equities.

Similar pressures could emerge in other markets that rely heavily on foreign capital inflows, including Vietnam.

Geopolitical risks add to uncertainty

Beyond interest rates, investors are also monitoring rising geopolitical tensions.

Renewed strains involving Iran, Israel and Western allies have raised concerns about the durability of ceasefire arrangements in the Middle East.

Any escalation could push oil prices significantly higher.

This remains a key concern because energy costs affect a broad range of industries. Rising oil prices often contribute to higher global inflation, making it more difficult for central banks to ease monetary policy.

Investors are now closely watching upcoming US inflation data, including CPI and PPI releases scheduled for this week.

Should inflation remain stubbornly elevated, expectations for prolonged high interest rates would likely strengthen further.

Challenges and opportunities for Vietnam

Domestic factors are also contributing to market caution.

Liquidity in Vietnam’s stock market has weakened noticeably over recent weeks, suggesting that both speculative and short-term investment flows are losing momentum.

At the same time, deposit and lending rates have shown signs of edging higher, while inflationary concerns and uneven domestic demand continue to limit fresh capital entering the equity market.

If the global rotation of capital away from emerging markets persists, Vietnam’s stock market may experience further volatility in the near term.

However, longer-term fundamentals remain supportive, including economic growth prospects, public investment expansion and the country’s ongoing efforts toward market reclassification and upgrading.

For now, investors may need to adapt to a market environment characterized by significantly higher volatility than in previous months.

Manh Ha