|

|

An expansion in state budget has helped the country to effectively control its public debt.

|

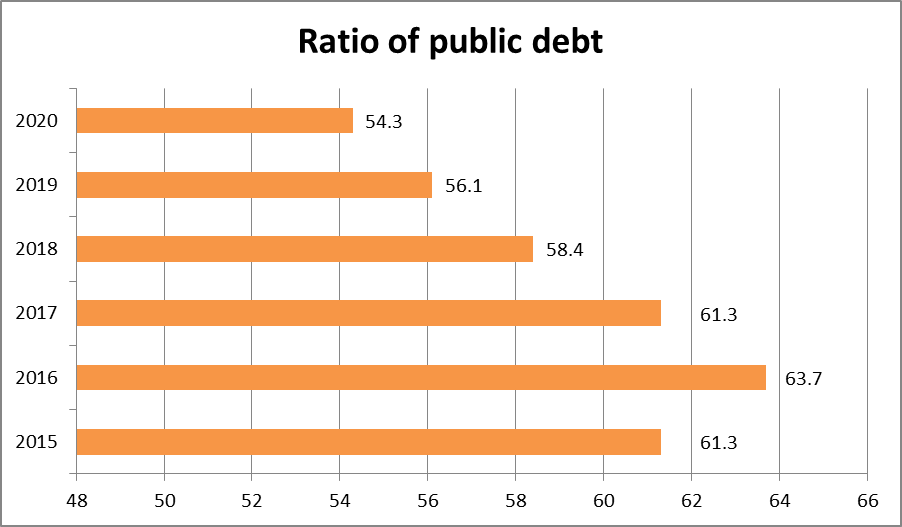

The government has reported to the National Assembly (NA) that the country’s public debt is estimated to be reduced to 56.1% of GDP, from 58.4% of GDP in 2018, and 64.6% in 2016.

This means that the public debt has been well controlled, ensuring national financial security, and is far lower than the permissible limit of 65% of GDP set by the legislature.

The Economist’s Global Debt Clock showed that, by last week, Vietnam’s public debt in GDP stood at 45.6%, and per capita public debt was US$1,039.67, while total public debt was close to USUS$94.85 billion. All the figures remained the same as they were in early 2019.

Under the existing Law on Public Debt Management, public debt includes governmental debt, government-guaranteed debt and debt accumulated by localities. The government-guaranteed debt embraces local and foreign debts held by state-owned enterprises and financial and credit organisations.

According to Francois Painchaud, resident IMF representative for Vietnam and Laos, in recent years, the Vietnamese government has successfully conducted significant fiscal consolidation, and strictly limited new issuance of government guarantees, reversing the swift increase in public and publicly guaranteed debt.

“Consequently, public debt fell to 55.5% of GDP at the end of 2018 from 60% at the end of 2016 (based on government finance statistics classification),” Painchaud said.

“Going forward, Vietnam’s debt-to-GDP is expected to fall further due to the authorities’ commitment to prudent fiscal policy, and also the forthcoming GDP revisions. This may help improve Vietnam’s credit rating, lowering its financing cost, which may also positively affect businesses’ financing costs.”

He added that in order to help limit future fiscal deficits, adequate revenue mobilization should be preserved, considering declining official development assistance (ODA), and oil and trade revenues. Although Vietnam is still enjoying favorable demographics, an acceleration of pension fund reform is needed to improve the coverage, adequacy, and sustainability of pensions.

Under IMF staff’s baseline, public debt would continue to decline to less than 50% of GDP in 2024.

Last month, Singapore-based ASEAN+3 Macroeconomic Research Office (AMRO), a regional macroeconomic surveillance organisation, released its annual consultation report on Vietnam, stating that a robust GDP growth of 6.6% this year and 6.7% next year, along with a tightened fiscal policy strictly in line with a five-year medium-term fiscal consolidation plan “would help contain public debt growth and reduce debt levels.”

Under baseline assumptions that the average GDP growth rate is at around 6.7% per annum, Vietnam’s public debt-to-GDP is forecast to gradually fall from 58.4% of GDP in 2018 to 57.4% this year, and to 54.6% by 2023, according to the report.

“The decline in the public debt-to-GDP ratio will contribute towards a larger fiscal space and help in increasing confidence in Vietnam’s macroeconomic sustainability going forward,” stated the report.

The government also has a good control of state budget revenue and spending.

In the first 10 months of this year, total budget revenue hit nearly VND1.14 quadrillion (US$49.6 billion), including VND45 trillion (US$1.95 billion) from crude oil exports, equal to 100.9 per cent of estimates. Meanwhile, total budget expenditure reached VND1.09 trillion (US$47.4 billion), including VND774.9 trillion (US$33.7 billion) in recurrent spending. Thus, the total budget surplus is US$2.95 billion.

Last year, state budget revenue and spending hit US$61.36 billion and US$71 billion, respectively, resulting in a budget deficit of US$9.64 billion or 3.6% of GDP.

Looking ahead, the government is likely to keep the budget deficit in 2019 below the target of 3.6% of GDP, given the relatively satisfactory progress in revenue collection, AMRO said.

However, last week, the NA adopted a resolution on state budget for 2020, with total state budget revenue of over VND1.51 quadrillion (US$65.65 billion), and total state budget expenditure of nearly VND1.75 quadrillion (US$76 billion).

Total budget deficit will be VND234.8 trillion (US$10.35 billion). Of which the central budget deficit will be VND217.8 trillion (US$9.47 billion) or 3.2 per cent of GDP, and the local budget deficit will be VND17 trillion (US$880 million) or 0.24 per cent of GDP.

According to Painchaud, recalibrating fiscal policy would also help support growth. Vietnam should consider a fundamental tax reform to help reduce economic distortions by broadening tax bases and narrowing tax incentives.

Vietnam’s large social and infrastructure spending needs – to address its sustainable development goals, climate change, population ageing and digitalisation – require the level and efficiency of infrastructure investment to be raised.

Clarifying the implementation of the anti-corruption law could help unblock public investment. Ensuring more effective competition in public procurement should be a priority in improving public investment efficiency. Nhan Dan

Thu Ha

Public debt continues with downward trend, Gov’t report shows

Vietnam’s public debt will fall to 56.1% of GDP by the end of 2019 from 58.4% last year, according to the Government’s latest report.

Fitch Ratings: Vietnam succeeds in lowering public debt

The Vietnamese Government has succeeded in decreasing public debt from 53 percent of GDP in 2016 to 50.5 percent by the end of last year, according to Fitch Ratings.