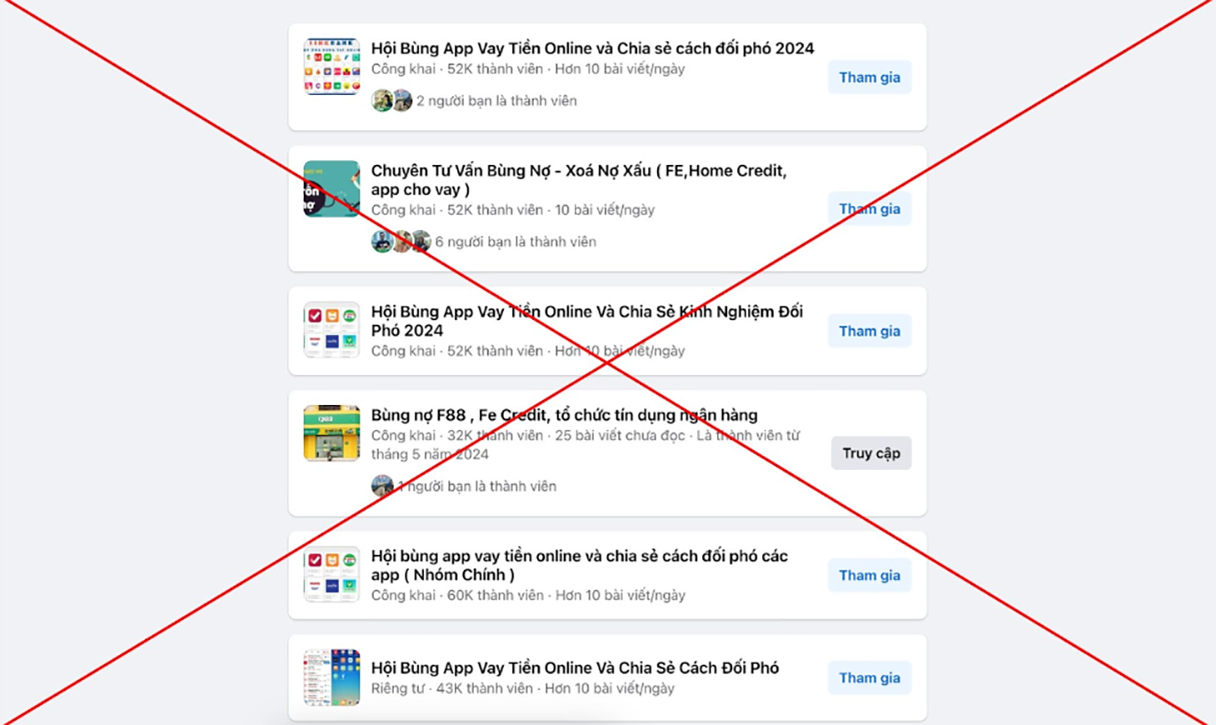

These groups quickly amassed large followings, with some, like "Expert Debt Dodging - Clearing Bad Debts (FE, Home Credit, loan apps)" reaching 132,000 members, and "Group for Dodging Loan Apps and Coping Strategies" attracting 107,000 members.

Daily posts in these groups provide tips and encouragement for members to avoid repaying loans from financial companies and loan apps, drawing dozens to hundreds of comments and likes per post.

Beneath the boasts of anonymous members celebrating their debt-dodging "achievements," lies the insidious promotion of new, easy-to-obtain loans. These new loan services often promise no face-to-face meetings, instant approval, no income verification, and no collateral. However, many who fall for these sweet promises end up trapped in a cycle of taking out new loans to repay old ones, with cumulative interest rates soaring to several hundred or even thousand percent per year, leading them into an inescapable debt spiral.

Lawyer Do Thi Hang from BFSC Law Firm explains that the rise of these debt-dodging groups stems from a belief that financial companies are reluctant to pursue debtors legally. However, financial companies do have legal grounds to sue defaulting borrowers. Initially, they may try to persuade debtors to repay by offering reductions or extensions. Persistent non-cooperation, however, will lead to legal action. Regardless of whether the debt is five or ten years old, debtors can still face criminal charges.

If taken to court and found guilty, borrowers might face fines, asset seizures, or even prosecution. Those inciting, guiding, or providing necessary means for fraudulent actions can also be prosecuted as accomplices.

Lawyer Hang emphasizes that financial companies generally prefer to avoid litigation. "Avoiding immediate responsibilities could lead to greater legal and social risks, especially with predatory lenders. Borrow only when absolutely necessary and within your repayment capacity," she advises.

As of April 2024, the Vietnam Banks Association reported that consumer loan debt from financial companies stood at approximately 138.8 trillion VND, constituting about 5% of the total consumer credit debt. Consumer credit debt accounts for roughly 21% of the total credit debt in the economy, amounting to nearly 2.9 quadrillion VND.

Navigating the debt maze: responsible borrowing in tough times

In 2023, the global economic downturn significantly impacted the income of many Vietnamese workers, particularly those in informal employment. According to Decision Lab, 30% of workers saw their incomes decrease by 10-50%, 21% consistently faced financial shortages, and 56% could only manage for one month without financial assistance. Amid this bleak landscape, many turned to borrowing as a solution.

However, borrowing is not straightforward for these workers, as those around them often face similar financial struggles. While 72% of respondents were willing to consider loans from banks or financial companies, 52% doubted their ability to meet the requirements, with income proof and lack of bad credit history being major obstacles. For many, bank loans were nearly impossible due to the lack of employment contracts or payslips, which are mandatory requirements.

In addition to banks and financial companies, the market also includes credit funds and pawn shops. Over the past year, pawnbroking has gained attention following police inspections of numerous pawn shops nationwide. These inspections revealed that pawnshops operate under clear regulations and legal frameworks, managed by the state.

To prevent debt from becoming a burden, both borrowers and lenders must act responsibly. Borrowers should only take loans that they genuinely need and can repay. Financial institutions have simplified procedures to make borrowing easier, which, while convenient, can lead to a debt spiral if not approached cautiously. Therefore, the advice "Borrow only when necessary" and having a clear repayment plan is often emphasized by lenders.

Dau Linh