With the listed price of VND43,200 ($1.9) per share, Vietnam National Petroleum Group (Petrolimex)’s market capitalisation stands at VND55.890 trillion ($2.46 billion), making it the ninth largest Vietnamese enterprise in this respect on the stock market.

However, as numerous Vietnamese blue chip stocks are losing their allure, Petrolimex’s shareholders have also raised questions about the firm’s long-term efficiency.

High dividend and worrying shareholders

Petrolimex was officially listed on the Ho Chi Minh City Stock Exchange (HOSE) under the ticker PLX on April 21, 2017.

Recently, investors have been paying attention to the corporation because of its dividend plan for 2016, which would hand out VND3.224 per share. This is an all-time record for Petrolimex.

If this plan is passed, except for the 155 million treasury stocks, it is estimated that Petrolimex will have to spend VND3.670 trillion ($161.48 million) on paying out this dividend, which is equal to 78.5 per cent of its profit.

People have also raised questions about the firm’s business efficiency within the next few years, especially as the world economy may produce unpredictable fluctuations which may directly influence oil and gasoline prices.

Moreover, the petroleum business in Vietnam faces many obstacles.

In the past, Petrolimex was once deep in the red. Present investors may expect a high dividend, but it is a short-term benefit only.

The long-term benefits lie in the core business lines of the firm and its ability to generate profit in many different market situations.

Petrolimex is a multidisciplinary group with a primary focus on petroleum business. The firm holds 48 to 50 per cent of the domestic market share with 2,400 retail stores and 2,800 agencies.

Of all domestic enterprises, it has the largest warehouse system, which have capacity of 2.2 million cubic meters, 570 kilometres of transportation pipeline, and a bonded warehouse that can house 150,000 DWT.

Besides oil and gasoline, Petrolimex also supplies lubricant, gas, petrochemical products, and holds stakes in banking, insurance, construction consultation, transportation, real estate, and so on.

These sectors contribute 40 per cent to Petrolimex’s revenue and about 50 per cent to its consolidated revenue.

By the end of 2016, Petrolime had 70 subsidiaries, one affiliate firm, and 13 associated companies. Some of these are well-known and listed on the stock exchange, such as Petrolimex Insurance Corporation (PGI), Petrolimex Gas Joint Stock Company (PGC), and Petrolimex Petrochemical Corporation (PLC).

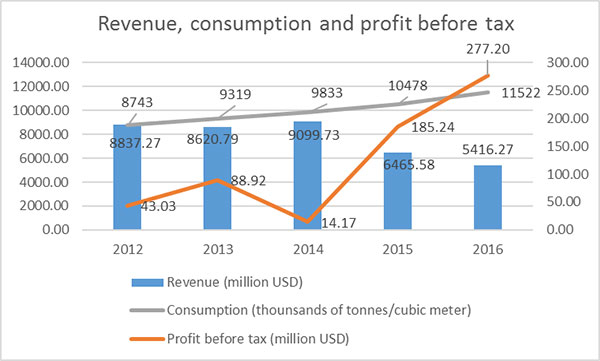

In 2016, Petrolimex supplied 11.44 million tonnes of oil and gasoline, an increase of 10.35 per cent compared to 2015, but due to the declining fuel prices, its net revenue was reduced to VND123.097 trillion ($5.42 billion), a reduction of 16 per cent.

However, thanks to the changes in the purchasing price formula calculation and a more suitable inventory policy, Petrolimex’s gross profit was improved from 8.7 per cent in 2015 to 11.5 per cent in 2016.

This led to an increase of 51.6 per cent in consolidated after-tax profit for the parent company’s shareholders.

The after-tax profit was VND4.669 trillion ($205 million), return on equity ratio (ROE) was 22.2 per cent, and return on assets (ROA) was 9.5 per cent.

Also, the growth of profit was derived from exchange rate differences.

In 2016, Petrolimex recorded a profit of VND56 billion ($2.5 million) from exchange rate differences, a huge boon compared to the loss of VND842 billion ($37 million) in 2015. 25-27 per cent of Petrolimex’s products were exported (mainly to Laos and Singapore) and these exports induced foreign currency income.

However, as it has to import its products, Petrolimex is affected heavily by currency appreciation.

In 2016, the 1.21 per cent increase in exchange rate difference, which was lower than the previous forecast of 3-4 per cent, and the State Bank of Vietnam (SBV)’s exchange rate management policy had an immensely positive influence on Petrolimex.

As of December 31, 2016, Petrolimex’s owners’ equity was VND23.2 trillion ($1.02 billion), an increase of 39 per cent compared to the beginning of this year.

Compared to 2011, the time of the company’s equitisation, its owners’ equity increased by 113.8 per cent.

This sharp growth originated from the rise in operating profit and the private placement of its strategic partner, which together reduced the liabilities to owners’ equity ratio to 57 per cent.

According to the plan awaiting approval at the annual general shareholders’ meeting on April 25, 2017, Petrolimex sets the target of VND143.208 trillion ($6.3 billion) in consolidated revenue, VND4.680 trillion ($206 million) of before-tax profit, and the minimum dividend of 12 per cent in 2017.

Leaders of Petrolimex said that the main obstacle is the rising competition. Some corporate clients now use gas or other fuels instead of mazut to minimise expenses and meet emissions requirements as well.

Moreover, Nghi Son Refinery will be put into commercial operation in the third quarter of 2017, Idemitsu Q8 will join the Vietnamese fuel market as a distributor and retailer, the exchange rate in 2017 may become unpredictable and fluctuate wildly, and Decision 49/2011/QD-TTg about emission standard application will also come into force.

All of these may raise the expenses of Petrolimex, while the market acceptance of new products is not clear.

To overcome difficulties, Petrolimex plans to restructure some of its businesses to be more compact.

The restructuring plan will start in the fields of oil and gasoline as well as transportation and mechanical-construction, while the company will be looking to conduct the private placement for its strategic shareholder Pjico and restructure PG Bank through the merger and acquisition deal with VietinBank, among others.

This restructuring initiative is one of the four main solutions that should be implemented to reach the annual target.

Unusually fluctuating revenue

The oil and gasoline business has a specific characteristic: the profit per unit sold is guaranteed when calculating selling price.

However, the accounting method first in, first out (FIFO), which is applied by Petrolimex, and the inventory period of about 30 days often make the import price adjustment later than the cycle of retail oil and gasoline pricing and adjustment in the domestic market, which is 15 days at present.

Thus, Petrolimex has to continuously take on risks from the global fluctuation of oil and gasoline prices.

Besides, Petrolimex’s profit structure is affected by its subsidiaries, affiliates, and associated companies.

In the fourth quarter of 2014, subsidiary Petrolimex Singapore suffered a loss of millions of US dollars due to the purchase of numerous oil and gasoline forward contracts.

As a result, Petrolimex’s profit of VND1.4 trillion ($61.6 million) in the first nine months of 2014 abruptly fell to a loss of VND9 billion ($396,000) by the end of the year.

In 2016, its subsidiaries’ profit recovered and accounted for 29.7 per cent of the total consolidated after-tax profit and 36.5 per cent of after-tax profit for the parent company’s shareholders.

In fact, with the large scale, various sectors, sources of funding, and being at the mercy of frequently changing factors, Petrolimex’s profit always sees unusual fluctuations, which makes it difficult for investors as well as professional analysts to reliably forecast its operating profit.

Expectations for the Japanese strategic partner

In the middle of 2016, Petrolimex has finished the private placement of 103.5 million shares (8 per cent of stakes) for strategic shareholder JX Nippon Oil & Energy Vietnam (JXEV), the subsidiary of JX Nippon Oil & Energy Corporation (JXE) from Japan. The offering price for JXEV was VND39,107 ($1.7) per share.

This private issuance earned Petrolimex VND4 trillion ($176 million), which increased its chartered capital and reduced its debts.

Also, state holding in Petrolimex was reduced to 75 per cent.

JXE is the biggest retailer of oil and gasoline in Japan, with a 43 per cent market share. Hitoshi Kato, vice chairman of JXE and a member of Petrolimex’s board of directors, said that JXEV will represent the Japanese parent company and supervise the activities of Petrolimex.

In addition, JXEV will provide management consultation for Petrolimex as a strategic partner and actively look for new business opportunities in Vietnam.

Nevertheless, there are some arguments that with only eight per cent of the stakes, it will be hard for JXE to have a voice in guiding Petrolimex’s activities.

Its participation in Petrolimex may be an exploratory move on the part of JXE to prepare for joining the Vietnamese market.

Otherwise, JXE should increase its stakes in Petrolimex so that it can have a voice.

In the 2017-2018 period, the state plans to reduce its ownership in Petrolimex to 65 per cent.

By 2020, this proportion will be 51 per cent only.

Petrolimex said that its strategic investor can hold up to 25 per cent of the stakes, but there has been no clear information on who this strategic investor is.

Based on the positive business results of 2016, earnings per share (EPS) of PLX is quite high at VND4,254 ($0.19).

The listing price of PLX was VND43,200 ($1.9) per share, so its average price to earnings ratio (PE) is much higher than that of other petroleum enterprises in Vietnam (7.98, according to Bloomberg).

On the OTC market, investors are excited to purchase PLX at VND50,000 ($2.2) per share, however, no one is sure whether this price can be maintained for a long time, especially when the VN-Index is on a decreasing trend.

Purchasing stocks means that shareholders believe in the firms’ future. PLX’s appearance on the HOSE will expand the Vietnamese stock exchange in terms of market capitalization, but expansion is not always good, especially if the firm cannot maintain its business efficiency after listing.

Leaders of Petrolimex are shouldering the pressure to maintain and even improve business efficiency to one-up 2016 standards.

Besides, Petrolimex shareholders will have to consider holding this stocks for the long-term, despite the many uncontrollable factors in the current business environment.

VIR