A Deloitte report showed that the number of convenience stores in Vietnam has expanded four-fold compared to 2012 and this segment made up the greatest share of new launches among types of shopping in the first nine months in 2018.

In addition, the compound annual growth rate (CAGR) of retail sales of convenience stores in Vietnam is 35.7%, much higher than the rest of Southeast Asia, according to the report.

Room for this shopping segment to grow remains large. The convenience store channel only accounts for less than 10% of retail sales in Vietnam, comparatively low compared to 20% in other developed economies. In terms of density, there is one convenience store per 54,500 inhabitants in Vietnam, also lower than figure for China and South Korea, 24,900 and 2,100 respectively.

Vietnam also has the fastest growth of middle class in Southeast Asia and attains extraordinary pace in the retail sector. This trend is predicted to persist in the future thanks to young population and rising purchasing power.

Not only did this shopping model attract large domestic corporations including VinGroup, Saigon Co.op, but also foreign companies namely Circle K, B's Mart, Mini Stop, 7-Eleven, GS25.

While Vingroup plans to launch more 4,000 stores of that kind by 2020, Saigon Co.op is acquiring small grocery stores mainly located in the countryside to expand its network. At the same time, giant retailer 7-Eleven aims to grow the number of stores by 1,000 within 10 years and Korean company GS25 targets to open 2,500 stores in the next 10 years.

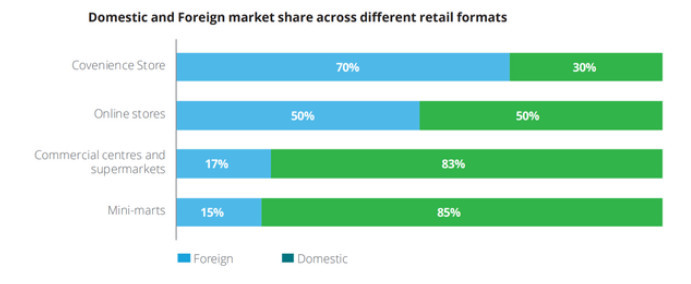

Domestic businesses seemingly still have the upper hand in the battle for market share, controlling 70%. According to Deloitte, as of January 2019, Vingroup alone had 1,700 Vinmart+ stores while the combined figure of foreign brands (excluding Shop&Go which has been acquired by Vingroup) stood at 600.

Source: Deloitte

Hanoitimes