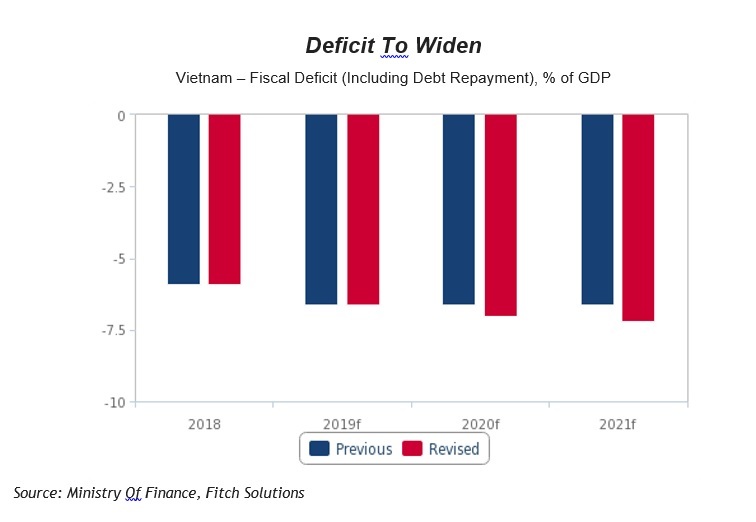

This follows the release of the Ministry of Finance’s three-year budget estimates in October, which indicates high debt repayments over 2020 and 2021.

Fitch Solutions forecasts are fairly in line with the government’s projections, given the government’s strong track record of meeting their fiscal deficit targets.

Risks to our deficit forecast stem heavily from debt repayment. A larger repayment than the government had initially forecast would see the deficit come in wider than we forecast, vice versa.

Excluding of debt repayment (to provide a like-for-like comparison with the government’s announced deficit projections), we are revising our 2019, 2020, and 2021 fiscal deficit forecasts to 3.4 %, for all three years, from 3.1%, 3.3%, and 3.5% previously. The forecasts are fairly similar to the government’s projections of 3.4 %, 3.4 %, and 3.5% for the respective three years, given a strong track record of the government in meeting their deficit targets.

|

Net of debt repayment, Fitch Solutions' wider deficit forecasts are informed by several headwinds to revenue collection, which it expects to persist over the coming years.

First, while Vietnam’s total trade will remain on a firm uptrend, supported by increasing relocation of manufacturing facilities from China, the country’s multitude of free trade agreements mean that revenue growth from import and export activities (14 % of total revenues) is likely to remain weak.

Second, it expects the equitisation process of State-Owned Enterprises (SOE) to remain sluggish, despite a revised lis t of companies in August, due to weak private sector interest, in part driven by the poor operating performance of most SOEs. Therefore, this segment will likely fail to contribute significantly to government coffers.

The Prime Minister issued Decision 26 /2019 on August 15 which provides a revised lis t of 93 SOEs which the government intends to ‘equitise’ by the end of 2020 . Decision 26 /2019 has replaced the previous lis t of 137 SOEs which was provided in Decision 58 /2016 as of August 15.

|

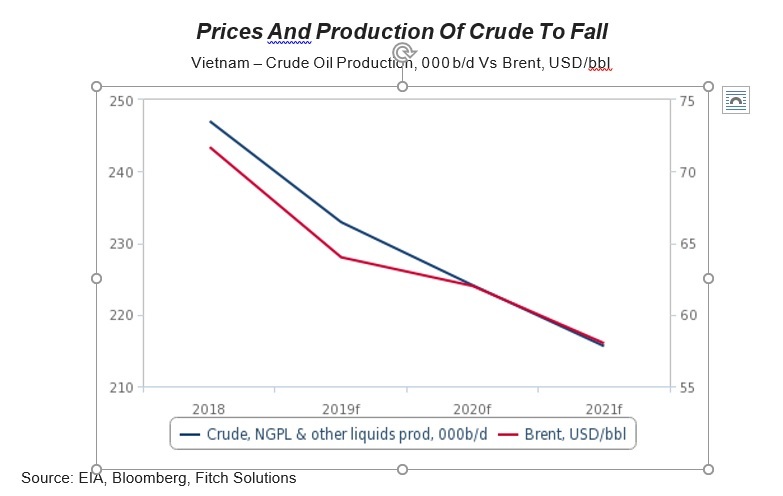

Third, crude oil revenue (2-3% of total revenues) will also weaken over the coming years. Vietnam collects a Natural Resource Tax from industries exploiting the country’s natural resources, including petroleum, minerals, and natural gas.

The tax rate ranges from 1-40 % and depends on the natural resource being exploited, and are applied to the production output at a specified taxable value per unit. Crude oil is taxed at progressive rates according to the daily average production output. Our Oil and Gas team forecasts Brent Oil prices to remain weak and also for Vietnam’s oil output to fall over the coming years (see chart above).

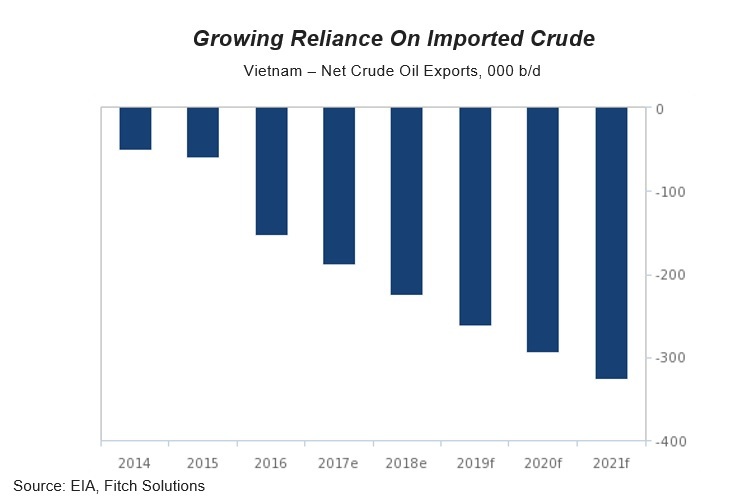

Additionally, the government has also removed a 5% import duty on crude oil from November 1 2019 , owing to an increasing demand for imported crude (see chart below). Both of these bode poorly for crude oil revenue over the coming years.

|

Fitch Solutions expects expenditures to come in fairly in line with the government’s projections. The Vietnamese authorities have historically demonstrated a strong track record of meeting their own spending projections and also meeting their deficit targets. This is despite signs during the year which suggest that expenditures may fall short of the annual target.

Expenditures attained just 64 .9 % of the budget estimate in September 2018 , but came in at 106 % of the budget estimate by the end of the year. Similarly in 2017, expenditures over the first nine months came in at just 65.1% of the budget estimate, but eventually reached 105% of the budget estimate at the end of the year.

The government’s strong track record of achieving their projections by year-end suggests that the trend is likely to repeat in 2019, where expenditures also just came in at 63.1% of the full-year estimate in September, and also over the coming two years.

Risks to deficit forecasts are evenly balanced. The government has tended to meet their revenue and expenditure targets for the year. However, one factor which could vary significantly is the level of debt repayment. A larger than initially projected debt repayment could see the fiscal deficit come in wider than our forecasts, vice versa.

Thien Van