In the past two years, numerous major technology and cloud companies have announced plans to build and operate new data centers across Southeast Asia.

While Singapore continues to lead the region, it faces increasing competition from Indonesia, Malaysia, and Vietnam, according to Adrian Ashurst, CEO of Worldbox Intelligence.

Data centers are crucial as they act as the physical “homes” for digital information stored in the “cloud” and other IT equipment, enabling services and platforms to function.

The rapid development of artificial intelligence (AI), cloud computing, e-commerce, and other technologies requires immense processing power and storage capacity, driving the demand for data centers.

Real estate investment strategy consultancy JLL predicts continued growth. In the next five years, data generated by individuals and businesses will double the amount produced in the past decade.

Data storage capacity at data centers and terminal devices is expected to grow from 10.1 zettabytes (ZB) in 2023 to 21 ZB in 2027, with an average annual growth rate of 18.5%.

Booming data demand fuels growth

Southeast Asia’s rapidly growing digital economies are driving the need for local data infrastructure. British real estate services company Savills cites Indonesia as an example:

"Of the 275 million citizens, 200 million have Internet access, and the online retail market is forecast to reach USD 95 billion by 2025. Indonesia is an emerging technology hub, with homegrown unicorns like GoTo raising over USD 1 billion when it went public in 2022."

A significant number of data centers have already been built in Southeast Asia, and regional governments are competing to attract more.

However, this growth also increases energy demand, which could strain already limited energy supplies. Data centers are known for being energy-intensive.

Singapore leads the way

Singapore’s strong infrastructure and stable energy supply have made it a top location for data centers in the region.

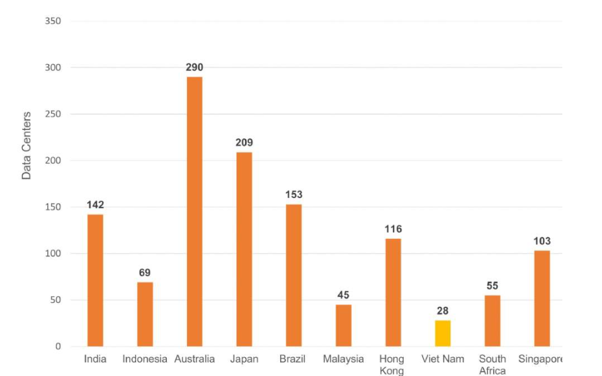

With over 100 data centers, it accounts for 60% of Southeast Asia’s total data center capacity. However, even Singapore is cautious about the impact on energy supplies and land availability.

In 2019, the government imposed a moratorium on new data centers (lifted in 2022) to assess the industry’s sustainability.

The country is now accelerating construction but has called for new projects to meet higher green standards. Data centers consume about 7% of Singapore’s total electricity, a figure projected to rise to 12% by 2030.

Though ranked among the most attractive locations for data centers globally - second worldwide and first in Asia - Singapore faces increasing pressure from countries like Thailand, Malaysia, Vietnam, the Philippines, and Indonesia, which offer advantages such as lower land and energy costs, along with growing investments in data centers by enterprises.

Malaysia closing the gap

Malaysia, currently home to around 50 data centers, is attracting investors with tax incentives and other privileges.

Iskandar Puteri City has emerged as a hotspot for data center construction, particularly after Singapore paused new projects in 2019.

The Malaysian government is working with energy providers to ensure a stable power supply for data centers.

In 2023, Kuala Lumpur unveiled the 2030 National Industrial Master Plan, which includes promoting digitization as a key growth sector.

Cloud giants like Amazon Web Services (AWS), Microsoft, and Google have all announced plans to expand their cloud regions in Malaysia.

Thailand sets ambitious goals

Leveraging its strategic location at the heart of Southeast Asia, Thailand—with around 30 data centers—made significant strides in November 2023 when Amazon, Google, and Microsoft agreed to invest 300 billion baht (USD 8.46 billion) in developing local data center infrastructure.

AWS plans to build a data center with a USD 5 billion budget over 15 years. Most recently, Google announced it would invest USD 1 billion in data center and cloud infrastructure in the country.

Indonesia’s advantages

By the end of 2023, Indonesia had about 73 data centers, with 16 more planned. Jakarta, West Java, and Batam have emerged as key locations, attracting both domestic and international investors.

The country benefits from abundant energy supplies and the potential for renewable energy development. A skilled workforce and booming demand for digital services are also significant advantages.

Indonesia’s data centers can also serve other markets, according to Savills. For instance, Batam Island near Singapore could become a future data center hotspot, meeting both domestic and Singaporean demand. Batam offers both traditional and renewable energy sources.

Vietnam’s growing appeal

Vietnam currently has around 30 data centers, with plans to build more in the coming years, driven by the rapid growth of its digital economy.

Savills notes that Vietnam’s cloud and data center industries are among the fastest-growing globally.

Key factors driving growth include digitalization among small and medium enterprises, a young and tech-savvy population, 5G development, the demand for digital infrastructure autonomy, and data-related regulations.

The Philippines on the fast track

The Philippines is home to about 22 data centers, with Manila being the top destination. The industry has recorded impressive growth.

In August 2023, the government announced that data center capacity is expected to increase fivefold, reaching approximately 300 megawatts (MW) by 2025.

Data centers are crucial for economic transformation. Building more data centers lays the foundation for Southeast Asian nations to drive faster economic growth in the coming decades.

Du Lam (Source: Febis, Savills)