From the outset, surging supply pressure sent the VN-Index plunging. After just a few minutes, the benchmark had dropped more than 76 points, while the HNX-Index fell 3.54 points and the UPCoM-Index slid 1.62 points.

The sharp decline was largely attributed to escalating tensions between the US - Israel and Iran, heightening concerns over geopolitical risks and potential disruptions to global energy supply chains.

Blue-chip stocks within the VN30 basket were hit hardest. Major tickers such as VHM, VPB, VRE, CTG and ACB at times fell to or near their floor prices, exerting heavy pressure on the broader index. The steep drop among leading stocks not only dragged down the main index but also triggered a ripple effect across other sectors.

Technically, the VN-Index is now retesting a key support zone around 1,800-1,830 points.

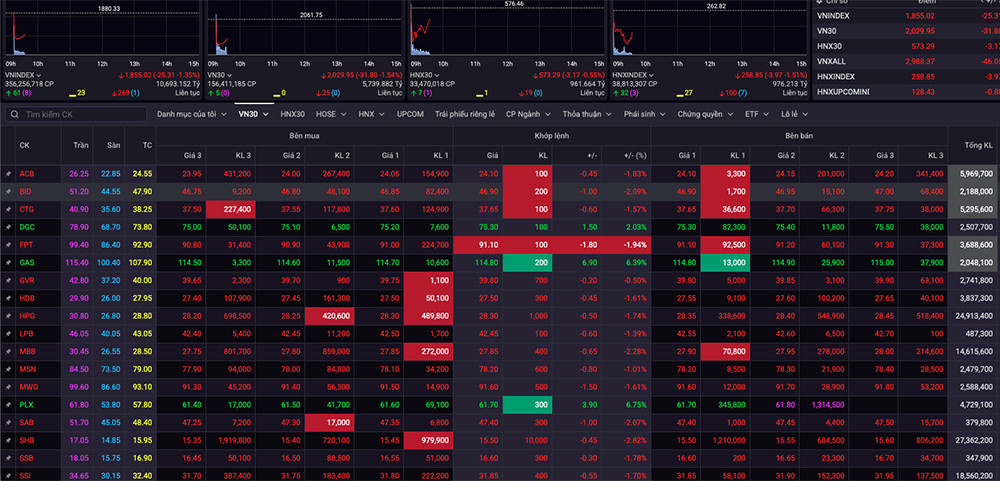

At 9:39am, the VN-Index was down 25.31 points to 1,855.02, a decline of 1.35 percent. The VN30-Index lost 31.8 points to 2,029.95, down 1.54 percent. The HNX-Index also weakened by 3.97 points to 258.85, a drop of 1.51 percent.

After a brief rebound, the VN-Index reversed course and slid deeper into negative territory. By the close on March 2, the benchmark had fallen 34 points to 1,846.

While most of the market remained under pressure, oil and gas stocks emerged as a rare bright spot. Shares such as BSR, PVD, PVS, GAS, PLX and OIL all hit their ceiling prices as Brent crude on the global market surged above US$80 per barrel.

GAS led large-cap gains, maintaining a high price of VND115,400 per share (approximately US$4.50), up 6.95 percent. On the HOSE, PVD advanced to VND41,300 per share (approximately US$1.60), marking a 6.99 percent rise.

PLX held firm at VND61,800 per share (approximately US$2.40), up 6.92 percent. PVS traded around VND52,100 per share (approximately US$2.00), gaining 9.92 percent, while BSR climbed to VND33,350 per share (approximately US$1.30), up 6.89 percent. OIL recorded the strongest increase, reaching VND21,900 per share (approximately US$0.85), soaring 14.66 percent during the morning session.

In contrast, banking and securities stocks faced steep corrections. After a prior rally, profit-taking combined with negative international news pushed many tickers such as VIX, HCM, FTS and VND to their floor prices or sharp losses.

HCM and FTS both hit their floor levels at VND23,700 per share (approximately US$0.93) and VND31,800 per share (approximately US$1.25), respectively, with no buyers in sight. VND fell 2.14 percent to VND18,300 per share (approximately US$0.72).

Real estate and steel stocks also succumbed to the downward trend. Capital flows appeared to rotate away from sectors sensitive to economic cycles toward safer assets such as gold and essential commodities.

Market volatility ahead

At the end of last week, the VN-Index closed at 1,880.33 points, up 56.24 points or 3.08 percent, supported by gains in VIC (19 points), BSR (7 points) and GAS (3.2 points). Over the week, the VN30 rose 2.1 percent, while mid-cap and small-cap indices rebounded 2.5 percent and 1.8 percent, respectively.

Market breadth was relatively positive, with 79 percent of stock groups advancing compared to 75 percent the previous week. Notable gainers included oil and gas (13 percent), chemicals (8.5 percent) and logistics (8.2 percent), while technology (-3.4 percent), real estate (-3.1 percent) and food (-2.3 percent) saw the steepest declines.

Total market liquidity in the week following the Lunar New Year reached VND34,083 billion (US$1.33 billion), up 34 percent from the previous week. Matched-order liquidity alone increased 47.5 percent to VND31,173 billion (US$1.22 billion).

According to MBS, the market may experience strong volatility, or even a correction, as it approaches the previous peak zone of 1,900-1,920 points, where significant liquidity - exceeding VND42,000 billion (US$1.64 billion) per session - had previously concentrated.

MBS recommends monitoring commodity-related stocks such as oil and gas, chemicals and fertilizers, natural rubber and minerals. Securities stocks are also worth watching as capital inflows show signs of picking up after a prolonged accumulation phase. In addition, retail, electricity production and distribution, and logistics sectors may benefit from the ongoing economic recovery.

Duy Anh