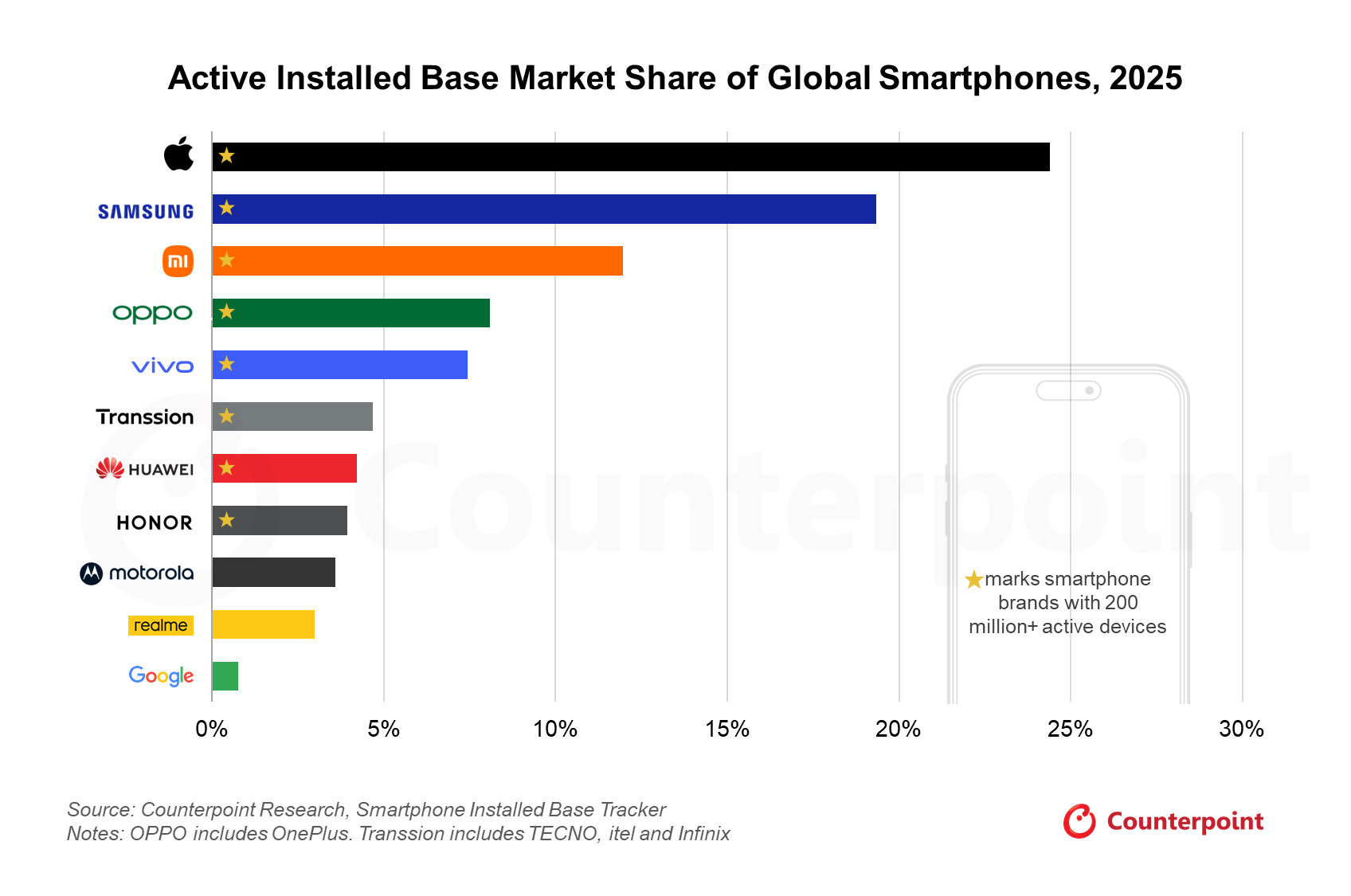

According to Counterpoint Research, 2025 marks a significant milestone for the global smartphone market, as the top eight original equipment manufacturers now each boast an active installed base of more than 200 million devices. Notably, nearly one in four active smartphones worldwide is an iPhone, while Samsung accounts for close to one fifth.

In a report released on February 10, Counterpoint said the global active smartphone base grew 2 percent in 2025. The main drivers were an extended replacement cycle of nearly four years and the continued expansion of the used device market. Rather than merely reflecting new shipments, the active installed base is considered a long-term measure of competitiveness, capturing user retention, product durability and ecosystem strength.

Within the “200 million club,” clear divergence has emerged. Research Director Tarun Pathak noted: “The top eight brands account for more than 80 percent of the global active installed base.” He added that these companies can be divided into three main groups.

The billion-plus group consists of Apple and Samsung, which lead thanks to premium positioning and tightly integrated ecosystems. They are also the only two brands to surpass one billion active devices in 2025.

The challenger group includes Xiaomi, OPPO and vivo, which have built large user bases in the mid-range and upper mid-range segments, competing through diverse portfolios and flexible pricing strategies.

The standout growth group is Transsion Group, including brands such as Tecno and Infinix, which focus on price-sensitive markets in the Middle East, Africa and Southeast Asia. HONOR is the latest name to cross the 200 million active device threshold, while Motorola and realme are approaching the milestone.

At the top of the table, Apple holds around 25 percent of the global active smartphone base. Senior analyst Karn Chauhan observed: “In 2025, Apple added more new users than the combined total of the next seven brands.” Samsung ranks second with roughly 20 percent market share, supported by a product lineup spanning entry-level to premium devices and a long-standing presence across multiple markets.

Combined, Apple and Samsung account for 44 percent of the global active smartphone base. Their advantage stems from longer replacement cycles, extended software support, higher durability and stronger resale value - factors that are increasingly important as users keep their devices for longer.

On the other hand, the premium segment, defined as wholesale prices above US$600, remains a major barrier for the rest of the market. The six brands outside Apple and Samsung each hold only single-digit shares in this category. Rising component costs and memory constraints are also putting pressure on premiumization strategies.

As artificial intelligence becomes the industry’s new focal point, competition is shifting from hardware specifications to software and ecosystem integration. On-device AI processing, productivity-enhancing features and seamless cross-device integration are seen as key tools for retaining users.

Counterpoint believes Apple is currently the only brand effectively leveraging its massive installed base to generate steady services revenue, turning each iPhone into a long-term monetization platform.

With replacement cycles lengthening and the market increasingly saturated, the global smartphone race is no longer about how many units are sold, but how many users are retained. In this long game, the gap between the leaders and the rest remains substantial.

Du Lam