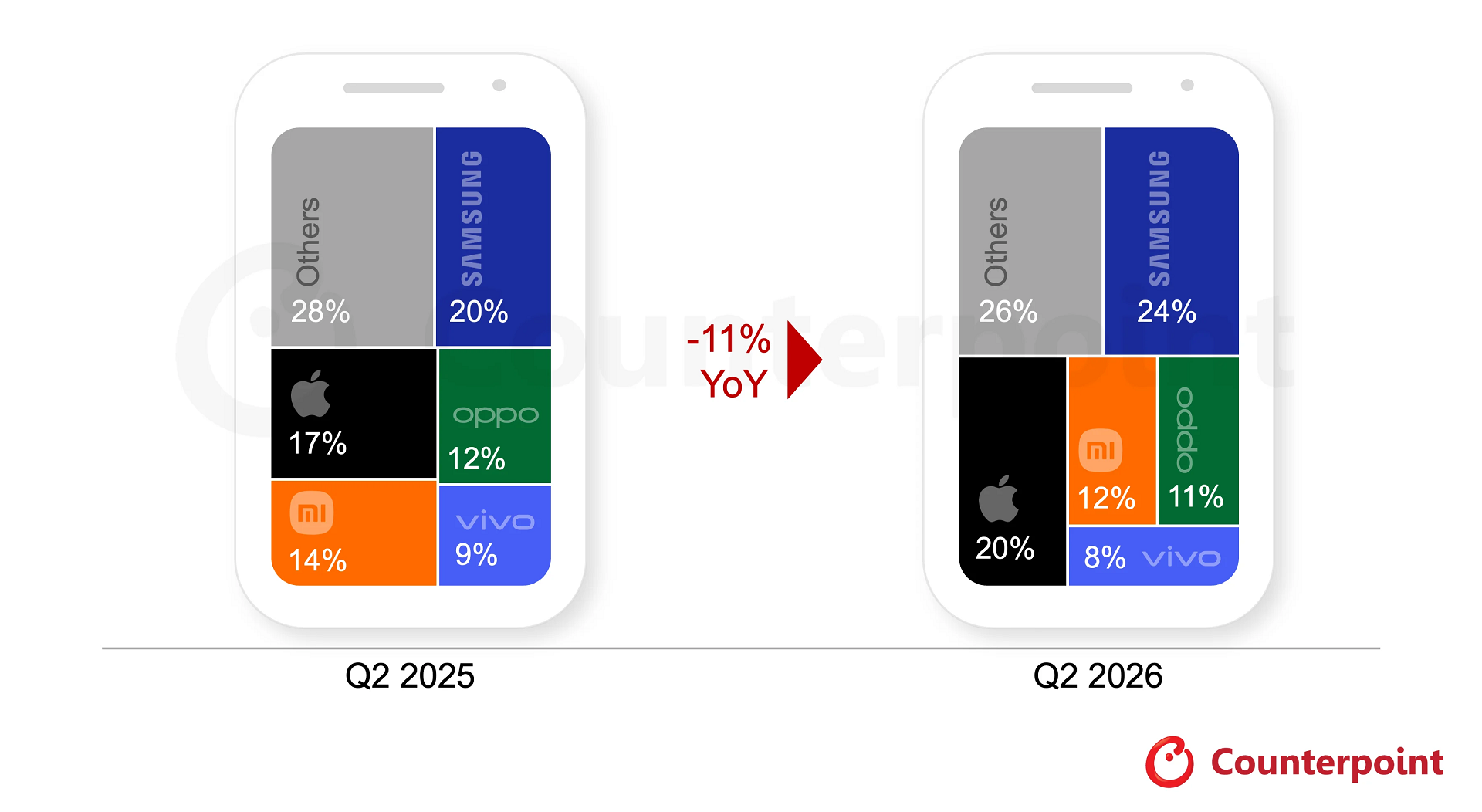

According to preliminary data from Counterpoint Research, global smartphone shipments fell 11% year-on-year during the quarter, marking the weakest second-quarter performance since 2013 as a severe memory chip shortage continued to disrupt the industry.

Memory shortage reshapes the market

The downturn has been driven largely by a global shortage of memory chips.

Semiconductor manufacturers have prioritised production of high-bandwidth memory (HBM) for artificial intelligence (AI) data centres, tightening supplies of DRAM and NAND chips used in consumer electronics and driving component prices sharply higher.

The surge in bill-of-materials (BOM) costs has hit budget and mid-range smartphones the hardest, where manufacturers typically operate on thin profit margins.

Chinese brands including Xiaomi, Oppo and vivo all recorded double-digit declines in shipments during the quarter, according to Counterpoint.

With product portfolios heavily concentrated in entry-level and mid-range devices, these manufacturers have been particularly vulnerable as consumers postpone upgrades, keep existing devices for longer or opt for older smartphone models.

"The global memory crisis has become the biggest headwind facing the smartphone industry," said Shilpi Jain, Senior Research Analyst at Counterpoint Research.

She noted that many affordable smartphones are "no longer economically viable at their previous price points" because of rising component costs.

To adapt, some manufacturers have increased retail prices, accepted lower profit margins, extended the life cycle of existing models, reduced hardware specifications or delayed new product launches.

Higher transportation and energy costs linked to geopolitical tensions in the Middle East have also added inflationary pressure, further weakening consumer spending.

Samsung and Apple outperform

In contrast to the overall market decline, Samsung and Apple both posted positive shipment growth, benefiting from strong premium brands and customer bases that are generally less sensitive to price increases.

Samsung regained the global lead with 24% market share, supported by 4% shipment growth.

Counterpoint attributed the performance to strong demand for the Galaxy S26 series, particularly the Ultra model, which features a privacy display and expanded AI capabilities.

Samsung also benefited from greater control over its component supply chain and aggressive summer promotions in key markets such as India and the Middle East.

Apple ranked second with a record 20% global market share.

According to Counterpoint, the iPhone 17 remained the world's best-shipping smartphone series during the quarter.

Apple was also the only major smartphone manufacturer that did not raise handset prices during the period, helping maintain strong demand across most key markets despite weaker performance in China.

Google and Huawei gain ground

Among other leading manufacturers, Google and Huawei also recorded shipment growth.

Counterpoint said Google expanded shipments by 16%, driven by strong demand for the Pixel 10 series, while Huawei posted 6% growth on the back of the Mate 80 lineup.

Counterpoint expects challenging market conditions to persist through the remainder of 2026.

The research firm forecasts global smartphone shipments will decline by around 14% for the full year, with memory shortages likely to continue into 2027.

As a result, demand for refurbished smartphones and older-generation models is expected to grow as manufacturers increasingly reduce their exposure to lower-margin entry-level devices.

Du Lam