The regional landscape is undergoing structural change. While Thailand, long the second-largest economy in Southeast Asia, faces mounting challenges from demographic aging to geopolitical volatility, Vietnam has emerged as a magnet for foreign direct investment and advanced manufacturing.

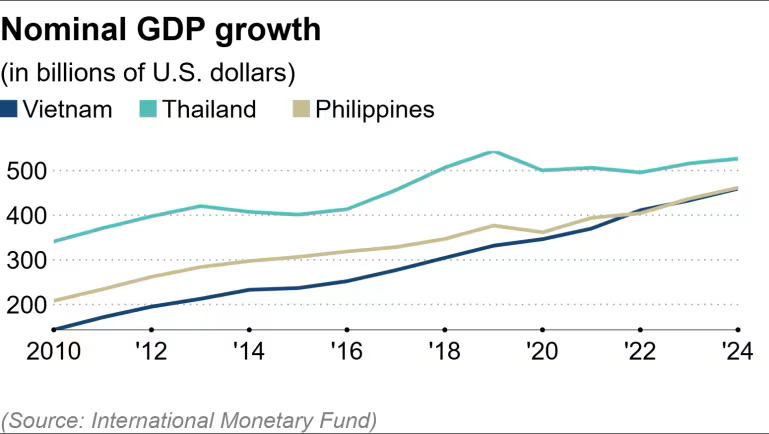

According to the latest data from Nikkei Asia and a report by Bangkok Bank, Vietnam is rapidly narrowing the gap and could surpass Thailand in nominal GDP as early as 2026-2027.

Vietnam accelerates on public investment and structural upgrade

Estimates show Vietnam’s real GDP growth reached approximately 8 percent in 2025. The government aims to sustain double-digit expansion from 2026 onward.

If this trajectory holds, Vietnam’s nominal GDP could approach US$500 billion by 2026 or 2027.

At that point, the country would overtake Thailand to become Southeast Asia’s third-largest economy, behind Indonesia and Singapore, with per capita GDP exceeding US$5,000.

The primary driver of this acceleration is an ambitious infrastructure strategy. The government has announced plans to invest the equivalent of 10 percent of GDP - around VND1.5 quadrillion (approximately US$60 billion) - in infrastructure projects between 2026 and 2030.

According to Nikkei, Can Van Luc, Chief Economist at the Bank for Investment and Development of Vietnam (BIDV), forecasts that public investment in 2026 will rise by about 26 percent, directly contributing 1.6 percentage points to economic growth compared to 2025.

A series of flagship projects is being fast-tracked, including Long Thanh International Airport, expected to begin operations in 2026, and new railway lines linking northern provinces.

At the same time, deep-sea ports and the North-South expressway network are gradually taking shape, transforming Vietnam from a low-cost assembly hub into a critical logistics node in the region.

Shan Saeed, Global Chief Economist at Malaysia-based property technology group IQI Juwai, believes Vietnam is entering a decisive phase of economic maturity.

The country’s competitive edge is no longer anchored solely in expanding low-cost manufacturing capacity. Instead, it is shifting toward structural upgrading.

High-tech sectors such as electronics, semiconductors, precision engineering and advanced components now account for more than 30 percent of total manufacturing output.

Vietnam’s electronics exports have surpassed US$120 billion, overtaking several regional competitors, including Thailand, in this segment.

Rapid integration into electric vehicle and advanced component supply chains is helping Vietnam narrow the technological depth gap with Malaysia and gain an advantage over Indonesia, which remains more dependent on commodity-related production.

Meanwhile, high-value services are expanding swiftly, supporting Vietnam’s transition toward a multi-engine growth model.

The services sector currently contributes around 42 percent of GDP, underscoring its increasingly important role alongside manufacturing.

With more than one million IT professionals, Vietnam’s digital and information technology services continue to record double-digit growth, gradually converging toward the service-led development model seen in the Philippines.

Thailand confronts economic headwinds

In contrast, Thailand faces significant constraints. The Organisation for Economic Co-operation and Development forecasts that Thailand’s real GDP will grow just 1.5 percent in 2026, down 0.5 percentage points from the previous year.

Since the COVID-19 pandemic, Thailand’s average growth has hovered between 2.7 and 3.0 percent.

Demographics pose one of the country’s most formidable challenges. With a median age of 40 - compared with 30 in Vietnam - Thailand is aging rapidly, leading to labor shortages and rising healthcare costs. High household debt is also weighing on domestic consumption.

The automotive industry, long a source of national pride, is showing signs of strain as Japanese manufacturers reassess their strategies.

In 2025, Suzuki Motor withdrew from automobile production in Thailand, while Honda Motor scaled back operations. Declining new car sales further reflect this shift.

In Indonesia, the region’s largest market, vehicle sales in the first 10 months of 2025 fell 10 percent, with Thailand experiencing a similar trend.

Beyond internal economic factors, geopolitical tensions have added pressure. Border frictions with Cambodia that began in May and escalated in December last year have disrupted bilateral trade and tourism flows.

Khang Vu, a scholar at Boston University, noted: “Geopolitical stability is crucial for sustaining growth in Southeast Asia. The Thailand-Cambodia border conflict exposes vulnerabilities that could unsettle foreign investors.”

Thai experts speak out

Vietnam’s ascent has sparked concern among segments of Thailand’s academic and business communities.

Dr Nonarit Bisonyabut, Senior Research Fellow at the Thailand Development Research Institute, warned that Thailand risks falling behind.

He argued that Thailand’s ambition to achieve high-income status by 2036 now appears distant, with revised projections potentially pushing the milestone to 2088-2093.

“Thailand once sought to catch up with China and Malaysia, which are on track to reach high-income status by 2025 and 2030 respectively. Now, we risk reaching that benchmark at the same time as Vietnam - around 2088 - despite having set our target decades earlier,” Nonarit said.

He also pointed out that Vietnam is pursuing decisive administrative reforms to enhance efficiency, while Thailand remains entangled in short-term or controversial initiatives such as cannabis liberalization and mega-projects lacking proven feasibility.

“Looking ahead, China and South Korea are prioritizing Vietnam over Thailand. Both countries are winners of the digital era, with China emerging alongside the US as an AI leader. Without serious reform, Thailand may lose its competitive edge and ultimately fall behind Vietnam,” he cautioned.

Kriengkrai Thiennukul, Chairman of the Federation of Thai Industries, likewise acknowledged that Vietnam is better positioned to capitalize on evolving global trade rules.

“Vietnam demonstrates stronger competitiveness, better skills and higher GDP and export growth figures. If Thailand talks without acting - or acts too slowly - we will lose our standing,” he stressed.

Poj Aramwattananont, Chairman of the Thai Chamber of Commerce, emphasized that Vietnam’s heavy investment in infrastructure is a key strategy to sustain growth and mitigate tariff risks.

Although he maintained that Thailand still retains advantages in geography and supporting industries, he admitted that investors remain hesitant amid policy uncertainty.

Observers also note that Vietnam is not without risk. Its heavy reliance on exports - holding the third-largest trade surplus with the US - leaves the economy vulnerable to tariff fluctuations, particularly under the administration of US President Donald Trump.

The OECD projects Vietnam’s GDP growth in 2026 could reach 6.2 percent, below the government’s target, due to potential export slowdowns.

Shan Saeed recommends that Vietnam focus on expanding profit margins, safeguarding intellectual property and digitizing logistics to avoid the middle-income trap.

Advancing up the value chain will require sustained investment in human capital and reliable energy infrastructure.

Southeast Asia’s economic future is being reshaped. While Thailand retains solid foundations in finance and healthcare, the pace and decisiveness of reform are propelling Vietnam forward, setting the stage for a remarkable shift in economic scale in the years ahead.

Du Lam